"Many Americans are too young to remember that the Great Depression was the result of a bubble bursting when a panic in the market caused the crash of stocks, real estate and commodities that had been bought by speculators with borrowed money."

"More recently, in the late 1990s, investors bid the stocks of technology companies so high - even those without any profits - that prices couldn't be sustained and the market crashed in 2000, triggering a national recession. The stock market still hasn't fully recovered."

"A recent study by analysts at the Bear Stearns & Co. Inc. investment bank in New York says most bubbles share the same characteristics: A strong economy and a sense of prosperity leads to speculation which leads to price pressures and a rise in interest rates which can lead to the bubble bursting."

"The analysts - Francois Trahan, Kurt D. Walters and Caroline S. Portny - believe that at least eight of the 10 characteristics of a bubble environment currently exist in America. But they are not surprised that few see it: "The idea that a financial disaster could occur at any moment is too far-fetched for individuals to imagine during times of such heightened exuberance."" [emphasis mine]

Sunday, August 28, 2005

Debt Warnings

News sites are covering a story warning of American's crushing debt burdens, especially here in California. It's a nice review. However, it's nothing new to us "bubbleheads". I appreciated the retrospective at the end; people never learn; maybe more of us should have stayed awake during history class:

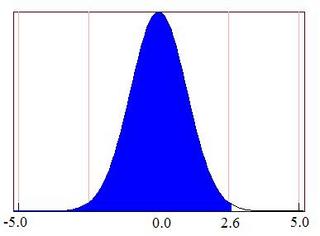

House Prices vs. Personal Net Worth

According to this article, today's median house value as a percent of net worth is 2.6 standard deviations (sd) above the median for the last 50 years. Keep in mind that this is a standardized distribution, so the fact that inflation, incomes, etc. have been going up over the last 50 years is irrelevant. Given a statistic like that (2.6 sd), how can people actually claim that house prices "make sense", "are justified", "will continue to go up", etc?

2.6 sd is huge. A value of 2.6 sd implies that the area under the bell curve below 2.6 sd accounts for 99.533881197628% of the total area under the curve. Do the math yourself if you don't believe me.

2.6 sd is huge. A value of 2.6 sd implies that the area under the bell curve below 2.6 sd accounts for 99.533881197628% of the total area under the curve. Do the math yourself if you don't believe me.

"What does that mean in English?"

"Try this. You can be a member of Mensa, the high IQ society, if your intelligence quotient is at least two standard deviations higher than the median, or normal, IQ. That's an unusual score because it puts you in the top 2 percent of the population."

"And that's where current home values are relative to everything else -- about two standard deviations up from the medians of the last half-century."

"The bottom line: Collectively, we're heavily mortgaged in a period of extreme prices. The return to more normal prices could be as painful at the Great Texas Real Estate Crash."

Friday, August 26, 2005

Fed Indicates Asset Prices Must Come Down

According to this article in Bloomberg, the Fed indicates in their latest remarks that there is an asset price bubble and that asset prices (e.g., housing prices) must come down for the sake of the economy.

Speculators*: be afraid, be very afraid. Why? For many reasons. A big one, as this article points out, is that in past housing busts the majority of owners had traditional fixed-rate loans and we didn't see a flood of houses on the market because many folks could just "wait it out" since mortgages don't get "called" like a put or a call in the stock market. But today "it's different this time", a significant number of people are using ARMs or exotic "name-your-own-payment" type loans; speculators certainly don't take out a fixed-rate mortgage because that just doesn't make sense if you are going to "flip" the property or you plan to sell in less than five or so years. But what is really scary is that in bubble areas like the Bay Area at large, such exotic loans are the majority because they are the only way most people can buy a house these days. These folks will get burned and the buy-up chain reaction will break down.

*I consider a speculator to be (1) anyone who buys a house other than the one they live in -- a vacation house, a house for "investment" reasons, etc., or (2) anyone who buys a property (regardless of whether it is the house they actually live in) with an ARM or exotic loan because these loans by their very nature are short-sighted and only make sense in an increasing asset price environment and are therefore speculative, or (3) anyone who decided to buy a house because "prices only go up, the rate of return on housing is greater than stocks", etc. and who would otherwise not have purchased a house. What do you, the three readers, think is the proper definition of "speculator"?

Some choice quotes:

Speculators*: be afraid, be very afraid. Why? For many reasons. A big one, as this article points out, is that in past housing busts the majority of owners had traditional fixed-rate loans and we didn't see a flood of houses on the market because many folks could just "wait it out" since mortgages don't get "called" like a put or a call in the stock market. But today "it's different this time", a significant number of people are using ARMs or exotic "name-your-own-payment" type loans; speculators certainly don't take out a fixed-rate mortgage because that just doesn't make sense if you are going to "flip" the property or you plan to sell in less than five or so years. But what is really scary is that in bubble areas like the Bay Area at large, such exotic loans are the majority because they are the only way most people can buy a house these days. These folks will get burned and the buy-up chain reaction will break down.

*I consider a speculator to be (1) anyone who buys a house other than the one they live in -- a vacation house, a house for "investment" reasons, etc., or (2) anyone who buys a property (regardless of whether it is the house they actually live in) with an ARM or exotic loan because these loans by their very nature are short-sighted and only make sense in an increasing asset price environment and are therefore speculative, or (3) anyone who decided to buy a house because "prices only go up, the rate of return on housing is greater than stocks", etc. and who would otherwise not have purchased a house. What do you, the three readers, think is the proper definition of "speculator"?

Some choice quotes:

"The Federal Reserve is paying closer attention to the rising values of assets such as stocks, bonds and homes, as low interest rates encourage more risk-taking, Fed Chairman Alan Greenspan said."The rest of the article is about Greenspan defending his economic philosophy and why he did the things that he did. CYA.

"Investors are accepting ever-lower compensation for risk as economic stability convinces them that their investments are less risky, he said. While that has helped push up asset prices and supported consumer and business spending, Greenspan said the increases ``can readily disappear.''"

"``History has not dealt kindly with the aftermath of protracted periods of low risk premiums,'' Greenspan said. ``Such an increase in market value is too often viewed by market participants as structural and permanent.''"

"``We have a housing valuation issue,'' said Kurt Karl, chief U.S. economist at Swiss Reinsurance in New York, in an interview. ``The time is now for raising interest rates and defuse these problems potentially by slowing down the economy a bit and avoid a big necessary increase later and a consequential recession. The froth here really raises the risk that he'll [Greenspan] continue to raise rates.''"

"``If we can maintain an adequate degree of flexibility, some of American's economic imbalances, most notably the large current account deficit and the housing boom, can be rectified by adjustments in prices, interest rates and exchange rates rather than through more wrenching changes in output, incomes and employment,'' he [Greenspan] said."

"Greenspan's comments come as a growing chorus of economists, including Stephen Roach of Morgan Stanley and David Rosenberg of Merrill Lynch & Co, have criticized the Fed chairman for remaining sanguine in the face of what they say is a dangerous bubble in the U.S. housing market."

"``We have experienced asset bubbles, and we now have an economy that is more highly leveraged than it ever has been in the post-World War II period,'' Kasriel said in an interview before the speech. ``Greenspan has been instrumental in bringing about this high leverage.''"

Thursday, August 25, 2005

Economist Predicts RE Bubble Bust for Early Next Year

CNNMoney is usually so bullish on RE, but this article is a refreshing turn; it reports an economist's opinion that the housing bubble is real and will bust as early as next year. Of course, economists always seem to be wrong and, naturally, we all know that Marin is special and it won't happen here, but it is interesting nonetheless.

Some choice quotes:

Some choice quotes:

"Soaring housing prices in the United States have created a real estate bubble that will likely burst early next year, Princeton University economist Paul Krugman said Thursday."

""I'll give you a forecast which might very well be wrong, but I think it will burst in the spring of next year," he said at a derivatives conference in Brazil's winter resort of Campos do Jordao."

"An expected decline in U.S. housing investment would be part of an economic adjustment process which could include the weakening of the dollar, higher U.S. exports and the reduction of current account deficits in the world's largest economy, Krugman said."

""This is how we would like to see it happening -- smoothly -- but there are many moving parts and they're unlikely to move at the same time," he said. "So it's not going to happen unpainfully.""

Are Today's RE Investors 'Parasites'?

In this Time article real estate investors/speculators are likened to parasites and the day-traders during the dot-com bubble, something us "bubbleheads" have known for some time. I would also include lenders and home builders to the rubric of 'parasite'. It also seems from this article that we've possibly entered the early stages of the finger-pointing/blame game.

Personally, I view today's RE investors/speculators more like locusts who move to some virgin territory, run up prices, destroy affordability, and then move on to some new locale without leaving any value behind.

Some choice quotes:

Personally, I view today's RE investors/speculators more like locusts who move to some virgin territory, run up prices, destroy affordability, and then move on to some new locale without leaving any value behind.

Some choice quotes:

"Randy Bianchi is a firm believer that in America, "a person should be allowed to buy a second, third or fourth home if he or she wants." That goes for real estate investors and speculators, even those who "flip" homes—that is, people who buy a house or condominium for the sole purpose of quickly selling it off for a profit, usually before construction is completed and often without even taking title to it. But Bianchi, a real estate broker and co-owner of Paradise Properties in West Palm Beach, Fla., who says he may soon flip a luxury condo himself, admits that his convictions about the practice are being tested in today's housing-price boom when homes in his area of Florida are jumping 35% a year. "Flipping," says Bianchi, "is turning into a negative phenomenon. In reality, it's pushing the market up too fast.""

"Some of the nation's leading homebuilders call that an understatement. To them, real estate investors, especially flippers, are to the housing boom what day traders were to the disastrous dot.com craze: a scourge distorting the market. In fact, Steve Hilton, co-CEO of Meritage Homes Corporation in Plano, Texas, said in an interview last month with the Arizona Republic in Phoenix—one of the nation's hottest real estate markets—that many investors today are "parasites" who artificially "raise the price of housing" but "don't bring any value." Craig Robins, head of Dacra Developers in Miami, concurs: the investors, he says, are bringing a hyper-short-term mentality to real estate ownership that creates too much turnover and "diminishes both the financial and community integrity of any development.""

"Investors argue they're being unfairly scapegoated. Developers, they say, are simply frightened that outsiders like them are getting a piece of the action for once. They add that homebuilders, far from being the socially conscious lot they've cast themselves as in this dispute, are just as culpable with respect to skyrocketing housing prices."

"What's also at stake, say the developers, is the status of the "home" as something more than a commodity as instantly tradable as pork-belly futures. When the prime purpose of a house or condo becomes hedging instead of living, they argue, it eventually loses the cachet of residential and community stability that keeps property values strong in the long term."

Tuesday, August 23, 2005

Condo Market Showing Signs of Weakness

According to this article, the condo market is on its way to popping. Condos are the last to go into a frenzy during a RE bubble. But what got me was this quote from the head RE cheerleader, David Lereah (emphasis mine): "Has the condo market peaked? 'Maybe,' said David Lereah. 'We may be seeing some of the air come out of the condo balloon.' "

So he is on record as claiming there is no housing bubble but given the latest facts the closest he can bring himself to saying "bubble" is "balloon".

So he is on record as claiming there is no housing bubble but given the latest facts the closest he can bring himself to saying "bubble" is "balloon".

Monday, August 22, 2005

Affordability May Bust This Bubble Say Analysts

The lack of affordability in the California housing market (and elsewhere) will pop this bubble if nothing else does. The Marin housing market is as dependent on first-time buyers as is any other housing market as it is the first-time buyer that initiates the "buy up" chain reaction.

Some choice quotes:

Some choice quotes:

"Prices in the hot U.S. housing market are poised to decline as demand dries up due to the inability of first-time buyers to afford a home, a Merrill Lynch analyst said in a research report on Monday."Affordability, Congress revamping housing's tax incentives, declining sales volume, declining prices, China floating the yuan, mortgage rates increasing (if slowly), what else? All in all it looks bad.

""The housing market has become so stretched that the affordability ratio for first-time buyers, the folks who drive the incremental demand in the real estate sector, has deteriorated to levels last seen in the third quarter of 1989," wrote David Rosenberg."

" The price of an average starter home in the United States has climbed 14 percent over the past year, while the average income for the first-time buyer family has risen just 4 percent, Rosenberg said, calling that an "unprecedented gap.""

"In the third quarter of 1989, bids evaporated and new home sales dropped 20 percent the following year in response to lofty prices that first-time buyers could not afford, the analyst said."

Congress Considering Reducing Housing's Tax Advantages

I woke up this morning and found this eye-opening email alert in my inbox; apparently Congress is looking into revamping the tax advantages presently enjoyed by mortgages. This is intended to remove the tax incentive of owning a house. This would destroy the current housing bubble if passed and just the rumor of it might be enough. On the one hand I think that there is no way this will ever pass as our politicians are too spineless. On the other hand, all districts would lose so maybe, since everyone is in the same boat, it could pass. Then there is the fact that the US is basically broke and needs to find new revenue streams and as always that comes from the peoples' pockets.

I was also struck by this comment: "I believe the tax catalyst has been essential and in fact we would not have had the housing boom of the last five years without the [tax code] changes in 1997.'' So they are now admitting that this housing bubble has not been driven by a housing shortage, by increasing fundamental value, etc.?

Some choice quotes:

I was also struck by this comment: "I believe the tax catalyst has been essential and in fact we would not have had the housing boom of the last five years without the [tax code] changes in 1997.'' So they are now admitting that this housing bubble has not been driven by a housing shortage, by increasing fundamental value, etc.?

Some choice quotes:

"The status of housing as the least- taxed investment in the U.S., which has helped fuel an eight-year boom in real estate values, may be in jeopardy as a presidential commission considers changes to the federal tax code."

The panel...is studying options to lower taxes on many types of investments to meet Bush's goal of spurring savings and economic growth. Changes to housing-related tax incentives will also be considered, Jeffrey Kupfer, the panel's staff director, said in an interview."

"Economists say such policies would have the effect of eroding the relative advantage housing has enjoyed over other investments since 1997, when Congress effectively made most sales of primary residences tax-free."

""One of the pillars of strength of the housing market is the fact of the tax-advantaged nature of the asset,'' says Anthony Chan, a senior economist at JPMorgan Asset Management in Columbus, Ohio. "To the extent that you chip away at that, you would see housing somewhat negatively impacted.''"

"The 1997 changes [to the tax code whereby Congress allowed homeowners to exclude up to $500,000 in gains when they sell homes they occupy] "just released this tsunami of resources and wealth in the housing market,'' says Brian Wesbury, a former chief of staff for the congressional Joint Economic Committee and now chief investment strategist at Claymore Advisors LLC in Lisle, Illinois. "I believe the tax catalyst has been essential and in fact we would not have had the housing boom of the last five years without the changes in 1997,'' Wesbury said in an interview."

"In contrast, income from other forms of investment is taxed at higher rates, creating the relative advantage for housing. Investment interest is taxed at rates as high as 35 percent; the rate on dividends was the same until it was reduced in 2003 to 15 percent."

"It is this relative advantage for housing that may be called into question by the tax commission. Members have said at hearings that they are considering a wide range of ways to stimulate savings. The options range from cutting rates on dividends, interest and capital gains to streamlining current tax-free savings mechanisms for retirement, education and health care -- or even junking the income tax in favor of a system that taxes only consumption."

"The toughest issue to tackle may be the mortgage-interest deduction, which has long been viewed as politically sacred, former Treasury Secretary James Baker III told the panel in March. "This is a political exercise every bit as much as it is an economic exercise,'' he said."

"The panel may also consider a recommendation by the congressional Joint Committee on Taxation to repeal the deduction for interest on home equity loans, Goold says. The panel's recommendations may include reducing the $1 million cap on which mortgages qualify for tax incentives, she says."

Sunday, August 21, 2005

Bubbles and Priniting Presses and Unemployment, Oh My!

There is an article over at The Daily Reckoning that summarizes the sorry state we find ourselves in today. I've tried to filter out the author's humorous yet idiosyncratic filler from those parts that are most relevant to the housing bubble:

Kurt Richebächer... says that the bursting of a housing bubble is bad news, from both a theoretical angle and from "Evidence of sharply slowing economic growth" that is "accumulating by the week for Britain and Australia, both belonging to the Anglo-Saxon family of housing bubble economies. Flattened house prices in both countries have drastically curbed home equity withdrawal, essentially with prompt, drastic adverse effects on retail sales." And now everyone is looking at us Americans, because we, too, are one of these selfsame Anglo-Saxon countries that is in the midst (or end) of a gigantic housing bubble that even Alan Greenspan can see (he calls it "froth"), and he is on record as declaring that neither he or any of his friends can ever even SEE a bubble until after it bursts! So this housing bubble must be huge if even Greenspan can see one!

Mike "Mish" Shedlock at the WhiskeyAndGunpowder.com site have taken a look into the future... and say "Massive amounts of announced layoffs in the banking and telecom industries will start kicking in the second half of the year. Eventually, this will spill over and affect housing just as it has in the United Kingdom and Australia. The United Kingdom has just about finished year one of a housing bust, and Australia is well into year two." And China is trying to cool down a housing bubble there, too, which means that they will have a bust.

And the housing bust may be starting here, too. As one piece of evidence, in the newsletter View From Silicon Valley, they write that published reports show that in the local market "y-o-y volume declining faster than y-o-y prices are rising." Oops!

And it is not like we are in for some refreshing little breather from blazing economic growth. Dr. Richebächer calculates that "the U.S. economy's performance was by far its weakest of the whole postwar period. Measured by employment and wage and salary income, it was a disaster. In real terms, average gross weekly earnings are barely higher than in 2000."

And it's not like there is some glorious demand for labor, as Mark Faber can attest. "According to a research paper by the Federal Reserve bank of Boston," he writes, "unemployment is far higher (around 8%) than what the US government's statistics show." And he underscores the type of jobs being created lately by saying, "High paying jobs are being lost while low paying jobs are added."

So... Americans have not had any increase in their aggregate standard of living attributable to income growth. ...Dr. Richebächer [says] "Given minimal employment growth, it turns out that for the American public there never was an economic recovery over the past few years. To increase the family's living standard, higher borrowing was generally required, which was done with abandon."

Paul Craig Roberts, is a former Associate Editor of the Wall Street Journal, former Contributing Editor of National Review, and former Assistant Secretary of the Treasury during the Reagan administration;... he has taken a look at the employment numbers put out by the Bureau of Labor Statistics. Out of 207,000 new jobs that the report said were created, 26,000 of them were government jobs. The rest were in the "domestic service sector" which are food servers, bartenders, health care workers, social services workers, real estate agents, credit intermediation, transportation workers, retail clerks and wholesale trade. He also wryly notes that "There were 7,000 construction jobs, most of which were filled by Mexicans." But Americans exploiting the hell out of people is what we do best, so at least some things never change.

I saw a reprised Financial Intelligence Report on NewsMax.com, the one with Sir John Templeton, who founded the Templeton Funds, when he "first warned of these interest rate hikes and the coming housing bust. Templeton, considered to be one of the world's greatest investors, believes real estate prices in some U.S. markets could fall by an astounding 50 percent." Half! And that was a few of years ago!

To show you how intellectually barren the modern "science" of economics is, it is only necessary to read what Glenn D. Rudebusch, who is Senior Vice President and Associate Director of Research at the Federal Reserve Bank of San Francisco, wrote in his essay entitled "Monetary Policy and Asset Price Bubbles". Not once in the entire report does he make mention of the fact that asset bubbles are the result of excessive creation of excess money and credit by the Federal Reserve, which provided the financing for the damn bubble, and without the financing there would be no bubble in the first damned place.... even our brave heroes at the Fed have problems dealing with bubbles, because they want to merely painlessly deflate the bubbles, so as to not cause a drag on the rest of economic activity. Meaning a recession, or depression, or worse.

To this I say... "Hahahahaha!" This is the damned dream of every government in the history of the world! Painlessly expand money and credit, and reap nothing but benefits! Hahahaha! That is why they all tried to do it, and this is why they all failed, too.

[Greenspan:] "As yet, there is no bottom line on the appropriate policy response to asset price bubbles." Well, duh! That's because there ARE no ways to painlessly deflate bubbles, dunce! If there were, every government on the face of the damned planet would be actively creating bubbles with both hands, you freaking moron!

But, since we cannot seem to learn, then we have to pay. Fortunes will be lost and lives will be ruined. That is how bubbles deflate. And it is ugly, and it has profound and lasting consequences.

At FreeMarketNews.com we get the depressing news that the Russians, who, not that long ago, were just a bunch of stupid communists, are throwing off that collectivist nightmare, and are now in a position to rightfully get on our case about the unbelievably expensive, pork-laden transportation bill that Congress just passed and Bush signed. As FMNN writes, "A recently published PravdaRU article calls the $286 billion U.S. transportation appropriations bill 'remarkable' and claims the staggering size can only be justified if U.S. leaders are fearful that the country is heading for a Great-Depression-type scenario and have decided to revert to good, old fashioned Keynsian 'pump priming' of the 1930's variety.

"PravdaRU explains it this way, 'When massive unemployment put the USA on the brink of survival during the Great Depression of the 30s, the government started funding the development of the transport infrastructure. Highways, on which the government spent billions and billions of dollars, rescued the entire nation. When Adolf Hitler came to power in 1933, he mobilized thousands of the unemployed to build autobahns, which Germany is proud of still. The road construction gave a very powerful impetus to the revival of the German industry.' "

The article, by guys who were dumb commies not that long ago so their criticism of us stings bitterly, "makes the point that the U.S. economy may be in much worse shape than the American mainstream media has reported, with higher inflation and much higher unemployment than the official figures recognize - 'stagflation' might be an apt description."

Residents 'Stretching' to Buy in Marin

Marin's housing market is as dependent on first-time and "move-up" buyers as is any other housing market; in this respect Marin is no different and therefore it is at as much risk as any other housing market. This article in (surprisingly enough) the Marin IJ discusses just how at risk is this group of Marin buyers. Naturally, the IJ does not give serious attention to the potential downside of this nor what happens when easy credit goes away.

Some choice quotes:

Some choice quotes:

"The wallets of Marin residents might be fuller than those in much of the state, but people are still stretching themselves thinner than ever to afford homes here, a private policy research organization reported today."

"The study from the Public Policy Institute of California indicated that more than half of California residents who bought a home within the past two years spend more than 30 percent of their total income on housing. In the Bay Area, including Marin, that number is 44 percent."

""Even in Marin, where incomes are higher than in most places, people still have to stretch to get in because housing prices are so high," said Hans Johnson, the study's co-author and a research fellow at the institute."

"The median household income in Marin is $94,410, the highest in the state, according to joint tax returns filed with the state Franchise Tax Board in 2003. But the median home price is also far and away the highest in the state, at $910,000 for single-family homes and $806,000 for all homes in July, according to La Jolla-based DataQuick Information Systems."

"That's because most buyers in Marin are "move-up buyers," or those who have owned a home elsewhere already and have made enough profit in the sale of that home to move a level or two in the market, according to Leslie Gavin, a private mortgage banker with Wells Fargo Bank in San Rafael."

"Still, the June housing affordability index from the California Association of Realtors reported that just 10 percent of Marin households today would be able to buy a median-priced home in Marin. That's down from 12 percent in May and 13 percent in June 2004."

""Most of my clients are pretty comfortable," she said. "But sometimes you get a buyer who just needs to get in the market so badly that they're going to stretch themselves, which is not always the most comfortable position for someone to be.""

"In those cases, buyers typically finance 95 percent of the cost of the house and have a debt-to-income ratio - the percentage of income used to pay for the house - of above 40 percent."

"The income to home-prices ratio isn't much different than it was two years ago, Johnson said, but if mortgage interest rates rise and prices flatten or decline, the bet by homeowners going to great financial lengths to buy becomes risky."

Historical Data Shows all Housing Booms Followed by Busts

This New York Times article focuses on Robert Shiller, the man who identified and warned about the crash of the technology stock bubble and who now warns of the impending collapse of the housing bubble. Dr. Shiller has collected historical data (going back centuries) showing that housing boom periods are always followed by painful busts and, contrary to what an RE bull will say and certainly contrary to what any realtor will tell you, housing is not a particularly good investment over the long term as house price increases just track with the increase in wages/salaries.

Some choice quotes:

Some choice quotes:

"...Mr. Shiller is sounding the same warning for real estate that he did for stocks. In speeches, in television and radio interviews and in a second edition of his prophetic 2000 book, "Irrational Exuberance," he is arguing that the housing craze is another bubble destined to end badly, just as every other real-estate boom on record has."

"He predicts that prices could fall 40 percent in inflation-adjusted terms over the next generation and that the end of the bubble will probably cause a recession at some point."

"To Mr. Shiller, though, it is a question of history, not salesmanship. Most people have never looked at decades and decades of home prices, because such data have been almost impossible to find. Stock-market charts often go back almost a century. Housing charts typically start sometime in the distant decade of the 1970's."

"But Mr. Shiller has unearthed some rare historical housing data for other countries. Using old classified advertisements, he was then able to fashion a chart for the United States that goes back to the 19th century."

"It all points to an unavoidable truth, he says. Every housing boom of the last few centuries has been followed by decades in which home values fell relative to inflation. Over the long term, the portion of income that families spend on their shelter stays about the same."

"The beauty of the [Shiller index] is that it does a better job of capturing the experience of homeowners than a simple average of house prices does. That average can rise when a bunch of new McMansions get built, even if existing houses have become no more valuable. The Shiller index, by following the same set of houses over many years, tracks the actual financial return that houses produce for their owners."

"Again and again, the cycle repeats itself. But there is essentially no long-term trend, beyond a general rise in house prices that roughly matches gains in peoples' incomes. As Amsterdam became a global city and its population exploded, demand for homes increased - but so, too, did supply."

"PRICES have hardly become more stable over the last 400 years; in fact, they've jumped up and down more in the 20th century than they did during the 18th and 19th."

""A whole lot of the price increases you see in houses is imaginary, because it's just inflation," said Mr. Eichholtz, a professor at Maastricht University. "People say, 'I have a house. It protects me against the economic imbalances or misfortunes of the country.' The big lesson is that real estate does not give you the protection that people think it does.""

Saturday, August 20, 2005

Just Sit Right Back and Watch the Slaughter of the Housing Speculators

This article makes it clear that the so-called "demand" for housing is speculator demand. These speculators will get slaughtered unless they cash out now and bank their profits. Unfortunately, they just roll it into the next "great can't-lose-real-estate-always-goes-up-everyone-wants-to-live-here deal".

"These days, “Get Rich Quick” has been the mantra for too many people trying to cash in while buying real estate speculatively. With so much “free” money still flowing from the Federal Reserve, it has become a real estate speculator’s dream world. These so called speculators have purchased over 3 million residences, practically with their eyes closed, with the sole intention of flipping them like pancakes to the next guy, marked up 25 percent or more. However, signs are beginning to appear that indicate this game of getting rich quick may soon be over. "

" Less than 20 percent of Californians can now afford a home with a fixed rate mortgage. The Federal Reserve is still raising variable interest rates. In 2004, when the housing bubble was really gathering steam, the National Association of Realtors calculated that 23 percent of homes purchased were for investment, and 13 percent were for second homes. With housing prices in some markets rising 20 to 40 percent in the past year – and 50 to 100 percent or more since 2000 – buying a house on spec looked like a sure thing to make a quick profit. But this housing deck of cards, in an already over-heated market, could have a domino affect. Why?"

"Home sales run about 9 million a year (this includes housing starts of 2 million and existing home sales of 7 million). If over 20 percent of homes purchased are investor properties, it appears that practically all new housing starts in America are accounted for by speculative buying. If second home buyers are added into the equation, speculative and investment buying of real estate (not owning to live in) actually exceeds total housing starts!"

"Let’s look at the economics of a “poster property” in San Diego called Park Place. The New York Times reported recently that a one bedroom condo is being offered for $719,000. A prospective buyer would expect to pay about $3,775 a month for a mortgage, plus maintenance fees, taxes and insurance. These additional costs can bring the monthly out-of -pocket total to well over $5,000 a month, or $60,000 a year. However, a renter, who would benefit from the same granite countertops, hardwood floors and fantastic views, can rent a nearly identical unit for only $2,400 a month, or $28,800 a year. At these price levels, the speculator who bought in could run an annual negative cash flow of close to $31,000 if they were forced to rent because no buyers could be found."

"In looking at some cities with major price appreciation (New York, Boston, San Diego, Miami, to name a few), in today’s world it just doesn’t seem possible to buy a house or condo and expect to make an economic return renting it out! Nationwide, there are over 3.8 million vacant units available for rent. In some communities, the over-supply of rental units on the market has pushed the average rent down as much as 20 percent. There remains a surplus of rental units."

"In achieving this record home ownership, the following has occurred: Sub-prime buyers now account for more than 10 percent; Another 10 percent can only buy with a “negative amortization mortgage” (very popular in California where 40 percent of mortgages are negative amortization); Up to two-thirds of mortgages are Interest Only (“IO”) or Adjustable Rate (“ARM”); Second homes now account for 8 percent of mortgages; and, 38 percent of homes this year have been purchased with less than 5 percent down (if this doesn’t reflect scrapping the bottom of the barrel for homeowners, nothing ever would). Yet, household earnings haven’t kept up!"

"If housing speculators stop buying, who’s left to buy? The average American with a job has already bought. America has been creating new homes faster than new jobs, and it has been the home speculator, and second home investor, holding up the market for at least the past year"

"There is another “dark side” to speculating in real estate. Hundreds of thousands of units that have been sold in advance by developers to speculators. This method is used by developers so they can get the construction finance they need. The speculator is responsible for the purchase but he won’t actually “buy” the unit until the project is complete and the unit has a Certificate of Occupancy. Therefore, the sale will not be counted as a sale until the date of closing! (Moreover, the developer has gotten the speculator to sign an agreement preventing him from reselling the unit for at least a year – after the speculator has taken occupancy – so the developer won’t be selling against himself. This leaves the speculator holding the bag, but they seem willing to take the risk."

"It could get interesting over the next six months as interest rates continue to go up and thousands of high-priced housing units come on the market that have been artificially snapped up by the get rich quick crowd. It may pay to simply sit back and watch the slaughter from a distance and stay short some home builders and sub-prime mortgage companies."

Porous Baloon or Bubble?

Some folks liken the current housing situations on the coasts to a bubble, others to something akin to a "porous balloon". If you take into account the natural time-scale of the housing market then it could be considered a bubble. Bulls who argue against the bubble interpretation often fail to take that time-scale into account. What do you think and why?

Anyway, here is an article that briefly summarizes some reasons for a deflating housing bubble:

Anyway, here is an article that briefly summarizes some reasons for a deflating housing bubble:

"The most important indicator is probably the growing length of time "For Sale" signs are sitting on lawns across the country. The Wall Street Journal and New York Times recently published big-picture reports on that, but smaller papers, from New Hampshire to South Carolina to Palm Springs, Calif., had already presented the tiles for that mosaic. "This happens in every cycle," says Wellesley College economics professor Karl Case, who has published several studies of the housing market with Yale economist Robert Shiller. "The first sign [of a slowdown] is always time on the market and inventory.""

"Yet there are other, even tinier bubbles rising to the surface. New-home construction has plateaued in the past year, though at a high level. Mortgage applications have fallen in four of the past six weeks. The inventory of foreclosure properties rose nearly 5% in July, according to Foreclosure.com, and is up 10% in the past year. Sales growth at home-and-garden centers and furniture stores has slowed sharply from a peak in early 2004, according to Commerce Department data. As of the second quarter, Home Depot and Lowe's were still making money hand-over-fist, but their share prices have flattened in the past month, with investors worried that higher interest rates will hurt business. Furniture sales have fallen in three of the past five months."

"Another leading indicator could be a slowdown in the pace of new-home sales, says Richard DeKaser, chief economist with National City in Cleveland. Unlike homeowners, who tend to resist cutting prices, homebuilders are more willing to slash prices on brand-new homes to get rid of them, if they have to. "If a price adjustment is required, we will see it there first," he says. "My read there is that we may be seeing price-softening already in the process of playing out." The National Association of Home Builders' index of new, single-family home sales fell for the second straight month in August, matching its lowest level of the past year."

Friday, August 19, 2005

The Marin Lifestyle is For Sale

As I am feeling more irreverent than normal (and given that there is not much that is particularly new in the news vis-a-vis real estate, other than the fact that on both coasts inventories are up and sales are down as are prices), I decided to post this obscenity I found on a Marin realtor's web site:

I love the phrase they use "yet inviting to today’s lifestyle". Would that be a "lifestyle" of excess? Please, post your comments on what word you would use to describe this thing. And doesn't the owner know that McMansions have fallen out of favor?

I love the phrase they use "yet inviting to today’s lifestyle". Would that be a "lifestyle" of excess? Please, post your comments on what word you would use to describe this thing. And doesn't the owner know that McMansions have fallen out of favor?

Thursday, August 18, 2005

Marin's Median House Prices Down for July

Some one in the comments section of this blog posted a link to this article in the Marin IJ (thanks!) indicating that Marin's median single-family house prices are down for July, 2005. This comes in combination with the over 20% year-over-year drop in sales volume. It will be interesting to see what happens next.

Some choice quotes:

Some choice quotes:

"Marin's median single-family home price in July was $910,000, a 1.6 percent decline from June and up 13.6 percent from $801,000 a year ago, according to La Jolla-based DataQuick Information Systems, a real estate data information service."

"The percentage gain was the lowest year-over-year price appreciation in Marin since July 2004."

""It's evidence that the extraordinary period of higher-than-sustainable price increases is over," said John Quigley, a University of California at Berkeley economist who specializes in housing markets. "The rate of appreciation will be reduced and in some metropolitan areas, they will level off.""

"The volume of Marin home sales dropped for the sixth consecutive month in July, DataQuick reported. There were 408 homes sold in July, a 15.4 percent drop from 482 homes sold in July 2004, and a 10.1 percent decrease from 454 homes sold in June."

"Single-family home sales plunged 20.3 percent from July 2004, while condo and townhouse sales dropped 9.2 percent."

"That trend - and homes for sale spending more time on the market - could continue, Quigley said."

"...51 percent of agents responded that the market favored sellers in July, a dramatic drop from 96 percent who said the same thing during the first quarter of this year."

Wednesday, August 17, 2005

Study Finds Houses 'Extremely Overvalued'

Single-family houses are "extremely overvalued" says this study. No. Really?! You don't say? Could have fooled me (but apparently not this person). Not here though; Marin is special.

Some choice quotes:

Some choice quotes:

"Single-family home prices are "extremely overvalued" in 53 cities that make up nearly a third of the overall U.S. housing market, putting them at high risk of price declines, according to a study released today."

"The report, by Richard DeKaser, chief economist of National City Corp., examined 299 metro areas accounting for 80% of the U.S. housing market."

"DeKaser terms a market extremely overvalued if prices are 30% above where he estimates they should be based on historic price data, area income, mortgage rates and population density - a proxy for land scarcity."

"Based on those criteria, Santa Barbara, Calif., is the nation's most out-of-whack market, with houses 69% overpriced. Rounding out the top five: Salinas, Calif.; Naples, Fla.; and Riverside and Merced, Calif."

"The highest-risk markets are in California; Southern Florida; parts of the Boston area; the Long Island, N.Y., counties of Nassau and Suffolk; and Ocean City, N.J."

"The big culprit: in 85% of the cities surveyed, home-price gains outpaced income gains during the past year. In Bakersfield, Calif., prices rose 33% while incomes increased 3%. In 29% of areas, prices outpaced income growth by at least 10 percentage points."

"Just 2% of markets were in bubbly territory at the start of 2004, vs. 31% in the first quarter of 2005."

""For the U.S. as a whole, I expect we're going to have an orderly correction. But that doesn't mean it's going to be equally orderly in all places," DeKaser says."

Tuesday, August 16, 2005

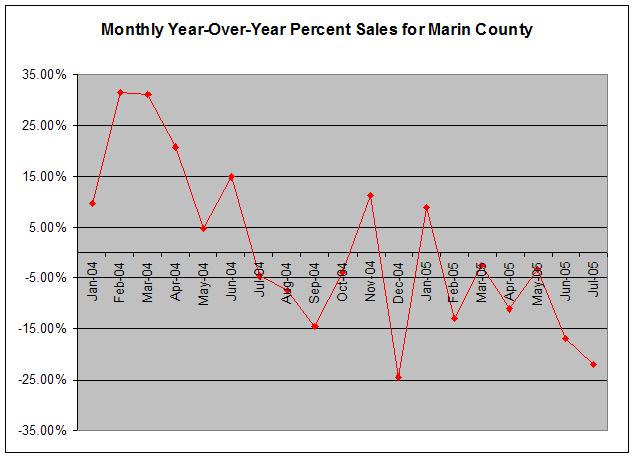

Marin Sales Results as of July [updated]

[Update: It turns out that I used the wrong July data for the second figure -- YoY percent sales were actually worse for July. I've updated the graph accordingly.]

No doubt by now you have read in other blogs that sales are down yet again across the Bay Area as is the home builder index. So that means it's time to post some charts for "God's country" updated for July (note that these results lag by a couple of months due to the time it takes to close a typical escrow).

The first chart shows that the number of houses put on the market in Marin County was very strong yet, as the second chart shows, percent sales remain firmly in negative territory (clicking on any chart will enlarge it).

No doubt by now you have read in other blogs that sales are down yet again across the Bay Area as is the home builder index. So that means it's time to post some charts for "God's country" updated for July (note that these results lag by a couple of months due to the time it takes to close a typical escrow).

The first chart shows that the number of houses put on the market in Marin County was very strong yet, as the second chart shows, percent sales remain firmly in negative territory (clicking on any chart will enlarge it).

{kind=link}

Monday, August 15, 2005

Housing Bubble, RIP

Continuing the theme of predicting the end of the housing bubble, this article makes some points worth considering but really nothing new to those of us who actually think. But of course, silly me, I forgot, Marin is special. It is immune to the laws of economics. Bursting RE bubbles are things that happen everywhere else, not here. It's "God's country" after all.

Some choice quotes:

Some choice quotes:

"The Fed Has Been Raising Interest Rates Now for 15 Months. To the Frustration of Fed Chairman Alan Greenspan, These Increases Have Coincided with a Continued Surge in Housing Prices and Activity."Surely the Fed is aware of the above mentioned dynamic. Yet, nevertheless, the fact that the Fed describes recent RE history as a conundrum possibly suggests that the Fed thinks "this time, it's different" and they expected a different response to their actions. Maybe what's different is that this RE bubble has NOT been fueled by improving fundamentals like rising salaries, better and more prevalent jobs, a brighter economic outlook, etc. and the Fed knows it and so expects a different outcome.

"Greenspan needn't regard this as a conundrum. As economist John Mueller has noted, when interest rates begin to rise, there's usually a surge in housing volume and prices for up to 12-18 months."

"That's because potential homebuyers, and especially speculators flipping homes or adding second or third properties to their portfolio, rush to lock in at low rates before they move higher. Anyone with an e-mail address has been bombarded with notes urging them to "act now" while mortgages are at historic lows."

"As rates reach their top, the opposite dynamic will set in over a 2-3 year period. A top in sales volume and prices, even a modest decline for a few months, will cause would-be buyers to wait."

"The Above Trends Have Been Fueled Synergistically in Recent Months by over-the-Top Aggressiveness by the Lenders and Homebuilders. The Share of Homes Bought with No Down Payment -- Zero Money Down -- Has Surged from Below 20 Percent Two Years Ago to About 40 Percent in Recent Months. Many of These Loans Were Combined with Teaser Interest Rates of 4-5 Percent."

"Those ARM loans, and the phase out of first-year rates, will, over the next year and a half, cause the monthly mortgage payment of many homeowners to rise by between 30 and 70 percent."

"The net impact [of policy tightening and new regulation] should be to put a ceiling on housing prices, and the stock prices of homebuilders and lenders. If the housing boom picks up for one last leg, regulators will be inclined to crack down on questionable practices. If inventory surges and prices decline even modestly, they may be forced to do so, or lenders may have to curb the excess on their own."

"Either way, like generals fighting the last war, regulators and lenders will likely be behind the curve -- acting, but too late, and defensively. This was the pattern during the S & L crisis of the 1980s."

"By next summer, there will be newspaper headlines and magazine covers, and congressional hearings, demanding to know why the Fed and Treasury allowed the bubble to grow so large -- and hence, made the correction so severe."

"Prices may not decline and could even rise in the Midwest, but on the overbought East and West coast -- which are also, note, heavy users of energy, and have crazy-high property and income tax rates -- there should be a nice price correction of say 25 percent."

"In the short term, markets, as George Soros have observed, seem to have a need for reflexivity. They "want" to go to excess. In the long run, of course, reflexivity works both ways. What`s gone up too much is likely to come down too much."

Spin

You just gotta love the spin that the RE bulls put in to this article from the LA Times; the SoCal markets are slowing big time yet it's all good news! This article raises so many red flags it's not even funny:

Red flag: "Southern California home prices hit new highs in July for the sixth consecutive month, even as pockets of slowing became more evident in certain parts of the region."

Red flag: "...the rate of appreciation has been essentially flat since the spring."

Red flag: " At the same time, the pace of sales continues to slow."

Red flag: ""Prices there are crossing the threshold at a much slower pace, but they're still crossing,...""

Red flag: " The Inland Empire also has started to see its torrid pace of price increases start to lose some steam."

Red flag: ""These things go in incremental baby steps and this is what you would expect to see in a normal real estate cycle,...""

Sunday, August 14, 2005

How Will It All End?

Even though I hold a Ph.D. from an elite university, my predictions in the previous post are nevertheless meaningless. This article, on the other hand, in the SF Gate, written by Michael Abrahams, Ph.D. (managing director at Hoefer & Arnett, a San Francisco investment banking firm, and an adjunct professor at the USF School of Business), is meaningful and furthers the theme of prognostication by asking "how will it all end?"

Some choice quotes:

And another article from the SF Gate by Robert B. Reich reiterates the China connection:

Some choice quotes:

"...the housing bubble is not just a Bay Area, let alone a U.S., phenomenon. Housing prices have been appreciating worldwide across markets of widely varying demographics, economic growth and location. Prices in South Africa, Hong Kong, France and New Zealand have been rising more quickly over the past year than in the United States."

"This boom has been heavily dependent on record low interest rates and, in the United States, a growing ability of borrowers to leverage their income. Because these low rates are a product of unsustainable economic events in the markets of international finance, interest rates and the ensuing housing bubble hang in a precarious balance."

"And where that trend in interest rates has reversed, as in the United Kingdom during the past year, prices have turned down. A U.S. decline is likely as well, particularly in markets such as the Bay Area, where price increases have been so strong and affordability is so weak."

"We appear to be repeating history: Interest-only loans were the dominant home finance instrument before the Depression. Sharply declining property values, coupled with the fact that the principle was never paid down, contributed to widespread foreclosures in the 1930s. That led to the introduction of the amortizing loan, in which the principle is paid off during the life of the loan."

"How will it end? Regulatory dissatisfaction with interest-only mortgages, rising interest rates and the financial inability of consumers to incur any more debt, or service existing debt at higher interest rates, may combine to end the housing party more rapidly than many expect."

"With consumers taking on record levels of variable-rate debt, many homeowners may find paying their debt, let alone increasing it to finance a more expensive house, difficult or impossible. In addition, a growing number of investors -- in place of owner/occupiers -- raises the risk of a more rapid price decline. Last year, 23 percent of all U.S. home sales were made to investors, who are driven by a need to profit from a house rather than simply to occupy it. Investors are much more likely to hit the exits when prices fall."

"While we should be able to watch the housing market bulls on "Flip That House" for some time, a year of two from now it will be running on the History Channel rather than the Discovery Channel."

And another article from the SF Gate by Robert B. Reich reiterates the China connection:

"China will let its currency rise against the dollar and America's housing bubble will burst."

"A major reason mortgage rates have stayed low is there's a lot of money around. And much of that money has been coming from abroad. China and the rest of Asia have been putting their spare cash into America, in order to prop up the dollar and make it easier for them to export to us."

"But that's about to change. We've been pressuring them to let their currency rise, and they're getting the message. We don't know yet how much they'll let it rise. But the writing's on the wall, in Chinese characters. And other Asian nations are following China's lead."

"You don't have to be a Zen master to see this means less money from Asia money flowing into the United States. Which in turn means long-term interest rates, including mortgage rates, will start to rise. It's just supply and demand -- less money around, and the cost of borrowing goes up."

"As a result, the housing bubble bursts."

"The moral of the story, as told to American policymakers who have been pressuring China to revalue: Be careful what you wish for."

Saturday, August 13, 2005

Predictions

To all three readers of this blog: How about anonymously posting your predictions of the time-line of the collapse of the housing bubble?

I'll go first. I'm by no means an expert or anything, I fully admit that I don't know anything useful, but for what it's worth (nothing) here's my prediction as of how it might unfold given how things look today:

I'll go first. I'm by no means an expert or anything, I fully admit that I don't know anything useful, but for what it's worth (nothing) here's my prediction as of how it might unfold given how things look today:

August - October, 2005

Interest rates keep rising and look to continue to rise into the foreseeable future. The sheeple who just want a place to live still buy, even more willing than ever to use risky loans, as mortgage rates are still relatively low. But overall, in the "hot" coastal markets demand continues to slacken and inventories are noticeably higher for this time of year. Oil makes new highs. House prices in "hot" markets make all new highs. Newspaper headlines still give lip-service to a housing bubble but the talking heads still claim that there is no bubble and prices will continue to increase. Speculators are unphased by anything and keep flipping.

November - February, 2006

In the coastal markets, demand continues to slow and inventories continue to increase. Fixed interest rates are entering uncomfortable levels. But the sheeple are distracted by Christmas shopping, the latest new car to show off to the neighbors, the romantic minutia of celebrities, etc. Since much of the money they have taken out of home equity has been spent, they take on even more debt. Oil makes new highs. Speculators continue to be oblivious and keep speculating.

March - July, 2006

Fixed rates are around 8%, maybe as high as 9%. Dreamers and speculators still think "houses always go up"; still rising interest rates, further decreased demand, and ever increasing inventories continue to be ignored by them as houses still look cheap to them and after all they have it all figured out how they can play the rates and loan types to their advantage.

August - October, 2006

Now the number of houses on the market for sale are legion and sellers are desperate; sellers finally perceive the immense "hole of debt" that they are responsible for and are desperate to sell hoping just to break even, never mind making a profit. Inflation is now acknowledged to be a lot higher than previously admitted. Oil is between $95 and $105 per barrel. Basic household items are now nearly 100% of last year's price. The sheeple are starting to wake up and groggily ask what's going on? Speculators still repeat their (now tiring) mantra that "houses always go up in value, people always need a place to live, everyone wants to live here, houses aren't like stocks,..."

October - December, 2006

"POP!" reads the newspaper headlines across the country. Now all the talking heads claim to have known it all along that there was a housing bubble and the blame game begins in full earnest. The mood on neighborhood streets is gloomy. No one is smugly talking about the value of their houses. Curiously, shiny new SUVs aren't as commonplace as they once were. Oil maintains its highs at around $100 per barrel. Speculators pause and take a moment to look around and see what the fuss is all about, shrug, and carry on.

January - December 2007

The US is defaulting and as a practical matter the dollar is clearly losing or has lost its status as a world reserve currency. Houses have lost 50 to 70% of their peak value depending on how hot the local market was at the height of the frenzy. Unemployment is rife in coastal states due to the fact that so many people were dependent for employment on the housing bubble. The bust of the US housing bubble is felt all over the Western world and their economies suffer as a result. The sheeple, if they haven't already, are buying guns, gold. The blame game is effectively over and now New Ideas are bandied around left and right as to how to fix the situation. Speculators are now broke and probably homeless.

2008

Hillary Clinton is hailed as the first female US president and "look how progressive we are, we truly are the leader of the Free World" and yadda yaddy and her administration inherits a country that is in a sorry state. The US becomes more aggressive and the rhetoric about "spreading freedom and democracy around the world" is more extremist. France, Germany, Britain, the whole of the EU politely turn their backs on the US and openly embrace the East. Iran, China, Russia, North Korea declare their camaraderie.

Friday, August 12, 2005

Marin's Population is on the Decline

Like much of the rest of the Bay Area, Marin's population is declining. I wonder why? Are they selling their over-priced, crappy little 70's era houses for a fortune and moving where? Or is it that kids who grew up here cannot afford to move back home? I guess it is not the case that "everyone wants to live here".

Some choice quotes:

Some choice quotes:

"Marin's population has dropped by more than 1,200 people in the past four years..."

"State demographer Mary Heim said the overall decline in Marin is attributable to Marin's aging population. State Department of Finance figures indicate that the number of deaths in Marin each year is inching closer to the number of births, a trend that should continue, Heim said."

"The state's latest predictions run contrary to what Marin planners had been anticipating."

"The state projections pointed to Marin as one of only seven California counties expected to lose population over the next 50 years while the rest of the state grows by some 20 million people."

Is Australia a Crystal Ball of Things to Come?

Normally, I try to focus on Marin County in particular and California in general. Well, the Marin IJ (our local news paper for those folks who don't live around here) is useless as a source of reliable information regarding housing here in Marin as it's "owned" by wealthy real estate developers, contractors, and other such vested interests and as such promotes their agenda. And of course our realtors, like realtors everywhere, spew whatever is in their best interests which always boil down to no matter what the market conditions are, "it's always a good time to buy; buy now before you get "priced out of the market"; everyone wants to live here; it's God's country don't you know", etc.

So sometimes I have to look abroad. Many people have claimed that the deflating housing bubble in Australia is a crystal ball of what is to come here in the US in general and in CA in particular. This article (focusing on Sydney) makes some refreshing points:

So sometimes I have to look abroad. Many people have claimed that the deflating housing bubble in Australia is a crystal ball of what is to come here in the US in general and in CA in particular. This article (focusing on Sydney) makes some refreshing points:

"This city's property addiction has turned toxic. House prices are falling; building approvals are down. The market is slowing, and as it does, it is weighing down the rest of the state's economy. New full-time jobs are rare in NSW, and their number is growing far more slowly than in other states. It is possible the state is in a recession."

"Home owners and property investors may not like the idea, but the real estate slowdown is a good thing - provided it is gradual enough not to cause serious problems for the rest of the economy. The task for governments, though, is to make sure the conditions which caused this unhealthy bubble are removed."

""The governor of the Reserve Bank, Ian Macfarlane, says the Sydney market is so distorted that it is in young people's interest to leave the city. It is simply too expensive to live here. While we cannot endorse that advice, the governor has rightly castigated the real estate industry's boosters who argue that the solution to Sydney's problem is to adopt policies that will lift prices again. High prices are the problem, not the solution.""

"It would seem that many Sydney people have anticipated Mr Macfarlane's ideas: for all that the State Government has been repeating its mantra that 1000 people a week are arriving to settle in Sydney (itself an overestimate), statistics on internal migration show that for every four arrivals in the state, three residents depart. A greed-driven, unsustainable housing boom creates an illusion of wealth while eroding the basis for sustaining it. What young person wants to live in a city where hopes of home ownership must forever be postponed?"

Safe as Houses

This opinion piece written by Paul Krugman in the New York Times describes the problem nicely in layman's terms.

Some choice quotes:

Some choice quotes:

"I used to live next door to a Russian émigré. One day he asked me to explain something that puzzled him about his new country. "This place seems very rich," he said, "but I never see anyone making anything. How does the country earn its money?""

"The answer, these days, is that we make a living by selling each other houses."

"So it's an economy driven by real estate. What's wrong with that?"

"...there's the disturbing point that we're paying for the housing boom (and the military buildup and tax cuts) with money borrowed from foreigners."

"...a fuller answer to my former neighbor would be that these days, Americans make a living selling each other houses, paid for with money borrowed from the Chinese. Somehow, that doesn't seem like a sustainable lifestyle."

"How solid, then, is America's economic recovery? The British have a phrase that applies: "safe as houses." Our economy is as safe as houses. Unfortunately, given current prices and our dependence on foreign lenders, houses aren't safe at all."

Thursday, August 11, 2005

Busy, Busy, Busy

I've been really busy at work and have not had as much time as I'd like to post to this blog. I just don't want all three of my readers to think I have abandoned this blog. ;)

I think there are only two news items of note lately. One is that mortgage rates are in their sixth straight week of rising. This is worth keeping an eye on.

The second is the ever deepening crisis at the GSEs. Fannie (Mae) 'stinks' and its stock is really getting a 'spanking'; it has been caught with its 'pants down' and it may never get to the 'bottom' of its problems. But seriously, given that much of the economy rests on the shoulders of the GSEs it is amazing to me that no one there seems to know what the heck is going on, financially speaking, in their company. Fannie Mae hasn't stated earnings for over a year and they say they won't be able to until sometime in 2006 and that furthermore the restated earnings are likely to reach over $11 billion (that's with a "B"). All I can say is "wow".

Here's an idea. How about if all three of you readers write a comment indicating the one single word that to you best describes the fiasco at the GSEs.

I think there are only two news items of note lately. One is that mortgage rates are in their sixth straight week of rising. This is worth keeping an eye on.

The second is the ever deepening crisis at the GSEs. Fannie (Mae) 'stinks' and its stock is really getting a 'spanking'; it has been caught with its 'pants down' and it may never get to the 'bottom' of its problems. But seriously, given that much of the economy rests on the shoulders of the GSEs it is amazing to me that no one there seems to know what the heck is going on, financially speaking, in their company. Fannie Mae hasn't stated earnings for over a year and they say they won't be able to until sometime in 2006 and that furthermore the restated earnings are likely to reach over $11 billion (that's with a "B"). All I can say is "wow".

Here's an idea. How about if all three of you readers write a comment indicating the one single word that to you best describes the fiasco at the GSEs.

Tuesday, August 09, 2005

NAR in Major CYA Mode

When the president of the NAR (David Lereah, aka "RE Cheerleader") comes out with a major CYA statement, buyers and sellers had better listen.

Some choice quotes:

Some choice quotes:

"Aug. 9, 2005--Home sales are expected to trend down from record levels during the second half of this year, but easily set annual records for both new- and existing-home sales, according to the National Association of Realtors(R)."This doesn't even make sense; so the housing market is going to tank but it's always a good time to buy or sell, basically to do whatever increases a broker's commission:

"David Lereah, NAR's chief economist, said home sales should be fairly stable in the near term. "The housing market is probably close to a peak right now in terms of sales activity, but there is tremendous momentum," he said. "Sales are expected to coast at historically high levels into next year, but they will trend slightly downward.""

""It's a great time to sell, but it may be a better time to buy about a year from now when the market should come closer to balance. However, postponing a purchase for another year would mean higher borrowing costs, so there are advantages to getting in now - it all gets down to a buyer's needs, resources and time horizons.""

Monday, August 08, 2005

Supply Far in Excess of Demand

This article in Financial Sense makes the case that available supply net teardowns far outweighs demand. I'm mainly just posting the figures, which are based on data from the US Census Bureau, as they speak for themselves:

"To maintain this rate, the new supply should be slightly more than 6% higher than the new demand. Thus, the supply running slightly ahead of demand is a normal thing. However, over the past 10.5 years, the supply (increase in total units) has exceeded the demand (increase in occupied units) by 35%! If we look at the last 3 years, the increase in the supply over the demand is 59.3%; and for the last 6 months it is in excess of 100%. At no time during the past ten years has there been any supply shortage. And it is not going to be the case over the next two years."

[The above graph shows] "the Supply-Demand mismatch with the supply being in far excess of the fundamental demand."

Are We In Stage 1 or 2?

The Boston housing bubble appears to be in stage 1 (denial) or 2 (anger) of the Kubler-Ross sequence.

"Sellers, many of whom are trying to cash out near the height of the market, are growing increasingly frustrated as their houses sit on the market for weeks and months."Meanwhile, San Diego, CA is just entering stage 1.

""The 'huge amount of inventory' is bringing prices down in Milton and Quincy, said Betsy Trethewey of Re/Max Landmark in Milton. Sellers are not acknowledging the changing dynamic, though, she said."

""Sellers are frustrated, and some are angry, she said. 'They've been very spoiled for the past few years. They're not accepting the truth of what is actually happening,' Trethewey said. Sellers traditionally are slower to realize when the market is changing, usually because their information is more dated than buyers'.""

" Nobody would pay San Diego prices without believing that prices will continue to rise."And from this article:

"Bubbles end when people stop believing that big capital gains are a sure thing. That's what happened in San Diego at the end of its last housing bubble: After a rapid rise, house prices peaked in 1990. Soon there was a glut of houses on the market, and prices began falling. By 1996, they had declined about 25 percent after adjusting for inflation."

"And that's what's happening in San Diego right now, after a rise in house prices that dwarfs the boom of the 1980s. The number of single-family houses and condos on the market has doubled over the past year. "Homes that a year or two ago sold virtually overnight - in many cases triggering bidding wars - are on the market for weeks," reports The Los Angeles Times. The same thing is happening in other formerly hot markets."

"Now we're starting to hear a hissing sound, as the air begins to leak out of the bubble. And everyone - not just those who own Zoned Zone real estate - should be worried."

"Flores, a self-described real estate "flipper," [in San Diego] is trying to sell two condos. But neither has gotten an offer after being on the market for more than a month, even though he's willing to break even on one and reduce the price on the other."

""It's getting trickier now," said Flores, 30, who became a full-time property investor three years ago after a short career as a senior financial analyst for a movie studio. "Everyone thinks this has peaked.""

"Once Southern California's hottest real estate market, San Diego County is feeling a real estate slowdown. It's a trend also starting to be seen in other regions..."

"San Diego has become a focal point of that discussion. People who believe the market is about to implode say that San Diego's cooling could be among the first signs of a pronounced downturn or even a possible crash in California."

"Amid concerns that prices might be peaking, more homeowners are selling, doubling the number of single-family houses and condos on the market from a year ago. Yet fewer are finding takers. Homes that a year or two ago sold virtually overnight, in many cases triggering bidding wars, are languishing for weeks."

Friday, August 05, 2005

Realtors Require Buyers to Acknowledge RE Can Drop in Price

Realtors now require buyers to sign a document that acknowledges that they (the buyer) understand that real estate can drop in price, sometimes precipitously. No more "real estate always goes up; real estate is always a great investment" nonsense. This is one of the more bearish thing I have seen of late coming from realtors; a last ditch attempt to protect themselves from the impending law suits as the bubble implodes.

Some choice quotes:

Some choice quotes:

"...real estate agents in some sizzling markets are asking consumers to sign a disclosure form stating that home prices can – and do – go up and down."

"In October 2004, the California Association of Realtors announced the release of a new disclosure form, the "Market Conditions Advisory," which states, "In light of the real estate market's cyclical nature it is important that buyers understand the potential for little or no appreciation in value, or the actual loss in value, of the property they purchase.""

"It is always problematic, she added, when homeowners lose equity. "They look for someone to blame. When the market has changed, there is no one to blame. We just want them to go in with their eyes wide open.""

""Because the market is so frenzied...what it's worth today has no reflection on what it's worth tomorrow""

Option ARMs are History

The second-to-last nail in the coffin of this real estate bubble is about to be hammered into place (the other "nail" being interest rates, which are rising). According to this article, option ARMs are going to be history very soon. Good riddance.

Some choice quotes:

Some choice quotes:

"On Aug. 1, Standard & Poor's blew the whistle on option ARMs. After an intensive study of recent mortgage-backed bonds, it concluded that lenders are allowing credit standards to slip too far. And too many of the borrowers using option ARMs are paying the minimum amounts per month, thereby accumulating potentially toxic levels of debt — especially in markets where home values are likely to soften."

"A second development potentially affecting option ARMs is under way at the federal financial regulatory agencies. A task force headed by Deputy Comptroller of the Currency Barbara Grunkemeyer is preparing new underwriting and credit risk guidelines on option ARMs, interest-only mortgages and reduced-documentation loans offered by the nation's lenders. In an interview, Grunkemeyer said the new guidelines could be out “by early fall,'' but there is no specific target date."

"Bottom line: It's probably sayonara to 125 percent mortgages at 1 percent to buyers with marginal credit, insufficient incomes, minimal down payments and no clue whatsoever about the potential payment-shock monsters lurking over the horizon."

Thursday, August 04, 2005

White House Not Bragging About Home Ownership Anymore?

According to this opinion piece, Bush is no longer spewing rhetoric about how Americans are so much better off now due to home equity. If so, what are they trying to tell us? And what about Greenspan's change of attitude regarding household debt, speculative buying, easy lending standards, froth?

"Already the White House has stopped inserting in President Bush's speeches the flowing rhetoric about how well off so many more Americans are because of equity in their homes. Perhaps we're jaded, but it seems even those evil TV ads for home equity loans are a little less frequent and intense."

Steep Decline in Self-reports of RE as Investment

Inman news is reporting a sharp decline in the number of folks who intend to purchase real estate as an investment over the next three to five years.

"Over the past 12 months, there has been a sharp drop in the percentage of investors across all age groups who plan to purchase real estate within three to five years, according to an annual survey released today by the MainStay Investments division of New York Life Investment Management LLC."

"In 2005, 13 percent of GenXers plan to add real estate, the survey found, compared with 32 percent in 2004, the study found. Five percent of Boomers plan to add real estate, compared with 18 percent in 2004. And 6 percent of Matures in 2005 plan to add real estate, down from 16 percent in 2004."

""Investors who change their investment approach – and shift assets as a result – based on the recent history in the capital markets are far more likely to do damage to their long-term financial well-being than those who follow a comprehensive financial plan," said Moore. "We're seeing a real disconnect between investors' attitudes and their lifetime goals. They're driving by the rear-view mirror.""

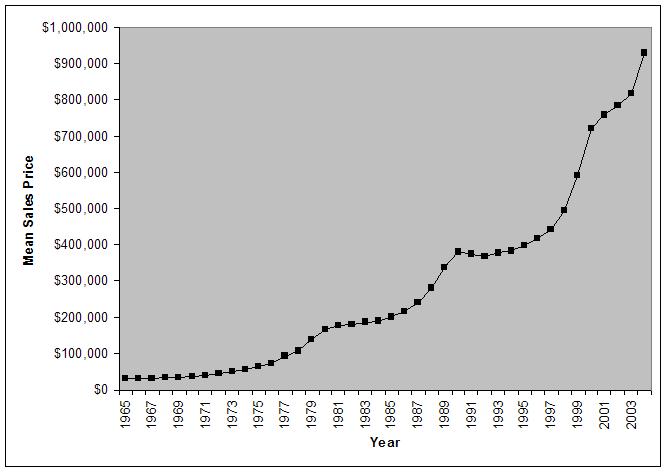

Mean Sales Prices in Marin

The following graph plots the mean sales price of units in all of Marin County, CA from 1965 to 2004. Click on the graphic to enlarge.

Wednesday, August 03, 2005