So you want more Marin-specific posts do you? Well, some of you do but most seem to be happy with the blog the way it is thank you very much. I'm not going to change based on the opinions of a minority, but here is one anyway just to make you happy. It is deliberately a bit inflammatory just to get the "thinking juices" flowing.

This is a letter I found in the

Marin IJ today. It was written by a Mill Valley resident. I reproduce it below:

Beware of proponents who promote their own surveys. I have no doubt that the majority of Marin and Sonoma residents who were polled by SMART about a sales tax increase to fund a rail transit system did so because they think it will solve the Highway 101 traffic problems.

A mass transit system sounds nice and the zero-sum equation of 4,800 rail riders equals 4,800 fewer cars on the road is attractive.

Such thinking is an urban legend unsupported by history. No urban or suburban county in this country that has deployed a rail or bus system has ever experienced a reduction in traffic congestion.

Mass transit and other commute improvements, such as adding highway lanes, simply add capacity to the transportation system, which fuels additional residential development on the outer edge, which adds more cars. Many of the same environmentalists who support a mass transit system for a corridor that does not have the population density to support such a system will ironically oppose the infill residential and commercial development that is necessary to create the required density of conveniently located jobs and housing.

Many of us are hoping the "other guy" will get out of his car and take the train.

A final fact: No mass transit system has ever been self-supporting based on rider fees (and maintained a frequency schedule that is useful).

So when it comes time to vote whether or not to tax ourselves for a boutique transit system, understand that the initial tax rate is only a fraction of what will be eventually required.

The writer makes some good points. It is difficult for a public transportation system to be profitable, but not impossible. And, all things being equal, if

all you do is increase the capacity of the transportation system then more houses will tend to be built thereby nulling the increased transportation capacity.

But what struck me as being just "so Marin" was the time-honored and unquestioned Marin provincial assumption that building housing is a Bad Thing. Why must that be a bad thing?

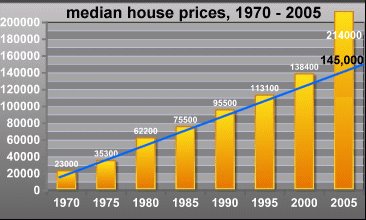

Marin has conducted this experiment (i.e., not improving transportation capacity) in tandem with draconian zoning rules (e.g., the Marin Agricultural Land Trust) for the last 30 years or so. It has resulted in the following highly visible consequences:

- Pathetically unaffordable housing (and all the problems it spawns)

- Crushing levels of traffic congestion (at least down the Hwy 101 corridor)

- A shameful offloading of the responsibility of housing our workforce to neighboring counties

- Tremendously long commute distances and times

And yet, people still move to Marin! New houses still get built in Marin and in neighboring counties although at a reduced (non-zero) rate. I submit that "the experiment" has only benefited long-time land owners and their real estate profits and has otherwise been an utter failure. In fact, I think profits are what it was really all about from the very beginning. I know for a fact that my Marin boomer parent who voted for MALT way-back-when admits that increasing real estate valuations was "definately a part of the equation". Flame away if you must but it's true all the same.

Some of the uglier and less tangible consequences of this failure is how Marinites have assumed an air of arrogance and superiority and a seemingly deliberate indifference towards the social consequences of unaffordable housing (of which much has been said on this blog and so I won't enumerate them here). We tend to turn a blind eye to the problems and claim it's someone else's responsibility.

I admit that this is a really gnarly and convoluted problem. But it has to be addressed. So what should be done? What do you suggest? Let's toss some ideas around in the comments section.

It seems to me that a part of the solution will have to involve an admission that people are still getting born and that they will need to live someplace near employment centers; some place other than

their cars. This is especially true if you believe in

Peak Oil.

Another part of the solution will have to involve taking responsibility for the mess that we find ourselves in and taking some real, meaningful action and not just lip-service. Exclusionary practices and NIMBYism are not the answer; we've tried that and it doesn't work.

Part of the fear Marinites have about building new houses is that they believe that it would result in urban sprawl akin to what can be seen in Southern California (which everyone in Marin loves to hate). I submit that there can be a happy medium between out of control sprawl on the one hand and no new building on the other. But to accomplish that will require revising MALT.

Well, have at it if you want.

The Novato Blvd. Index (NBI), where I drive the entire length of Novato Blvd., resulted in a total of 61 for sale signs.

The Novato Blvd. Index (NBI), where I drive the entire length of Novato Blvd., resulted in a total of 61 for sale signs.

{kind=link}

{kind=link}