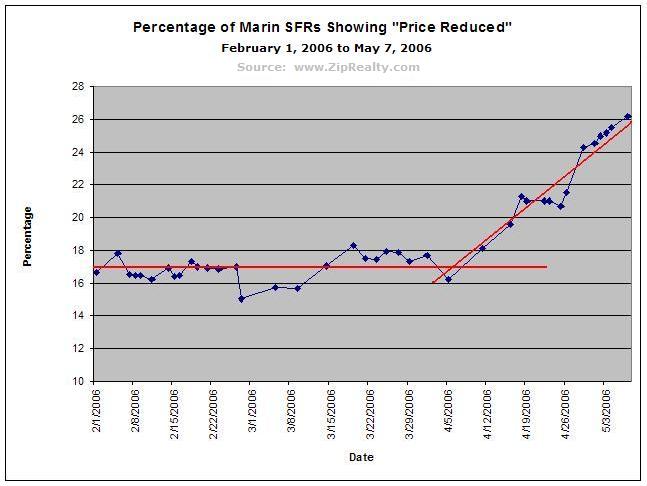

Well, I guess I am not alone afterall in claiming that strict environmental zoning and artificial land-use restrictions are counter-productive and socially disruptive. Further, despite our claims that we are oh-so-progressive, this article claims that such land-use restrictions are in fact anti-progressive.

Well, I guess I am not alone afterall in claiming that strict environmental zoning and artificial land-use restrictions are counter-productive and socially disruptive. Further, despite our claims that we are oh-so-progressive, this article claims that such land-use restrictions are in fact anti-progressive.Land-use restrictions were started, or so it is claimed by their proponents, in order to make the Bay Area more "livable" (insert your favorite intangibles here). To no one's surprise the artificially created scarcity of land has made housing unaffordable in the Bay Area and has no doubt inflated our egos to match ("Wow! I live in a million dollar 2 br 1 ba hill shack. We must live in the best place ever!"). This pathetic situation has only been exacerbated by the run-up due to the incredibly easy access to credit, exotic "toxic" loans, etc. all of which add up to the housing bubble mess that we are currently living in. But like this article says, "how livable is a place if you can't afford to live there?"

It was well known in the 70's (as attested to by my boomer parents and their friends who still live here) that these restrictions would primarily preserve if not increase land values and that was a big part of it. Property values clearly took precedence over building a healthy community, kids' education and development, social mobility, diversity, business, etc.

That was the choice made by the previous generation. But we don't have to sit idly by.

Marin County's (and others') land-use restriction policies are best summed up by the article as "a sad distortion of social priorities". As much as I like pasture land and trees, I couldn't agree more. It is at best an experiment that has gone awry. Flame away if you must, but someone has to ask the hard questions in public and it might as well be me and besides, what better medium than a blog?

The sooner that we acknowledge that a problem exists the sooner we can address it. I don't think more of the same can be tolerated. I'm afraid that if things do continue on as they have been then there may be no businesses left or the only way to make sufficient money to live here will be more frequent and more extreme boom-bust cycles, more get-rich-quick schemes (e.g., options), more who-knows-what.

Some choice quotes (emphases mine):

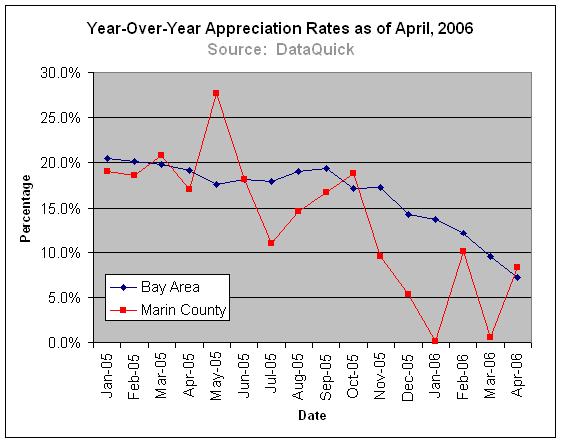

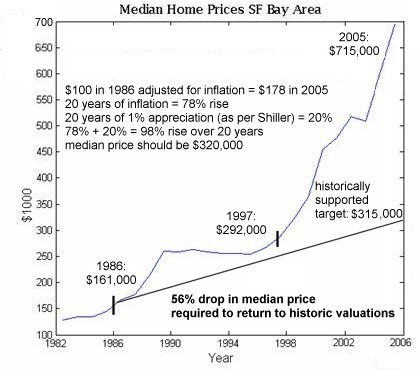

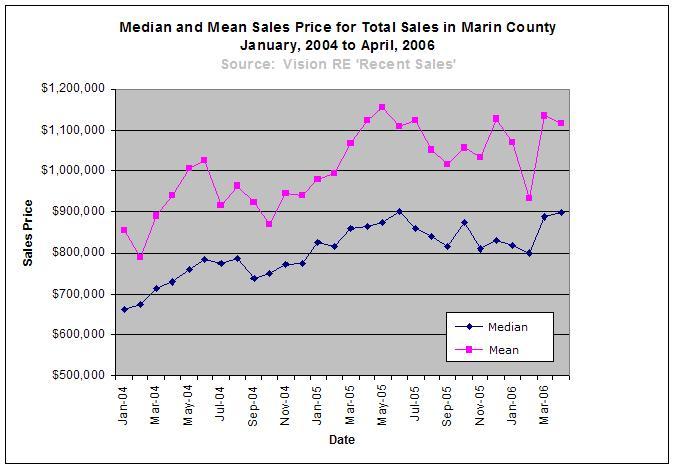

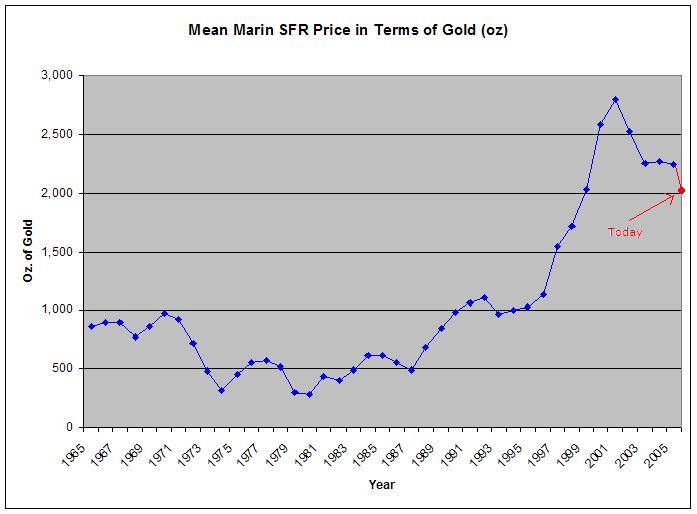

Most people know that the San Francisco Bay Area has one of the most expensive housing markets in the nation. However, not everyone realizes that, as recently as 1970, Bay Area housing was as affordable as housing in many other parts of the country.

Data from the 1970 census shows that a median-income Bay Area family could dedicate a quarter of their income to housing and pay off their mortgage on a median-priced home in just 13 years. By 1980, a family had to spend 40 percent of their income to pay off a home mortgage in 30 years; today, it requires 50 percent.

What happened in the 1970s to make Bay Area housing so unaffordable? In a nutshell: land-use planning. During the 1970s, Bay Area cities and counties imposed a variety of land-use restrictions intended to make the region more livable.

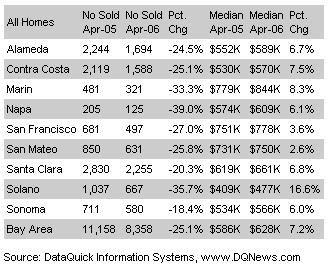

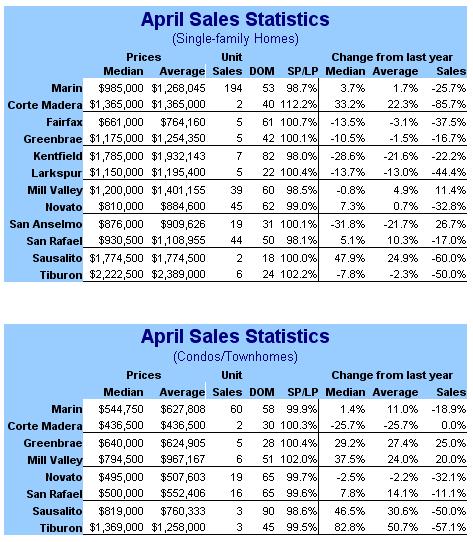

These restrictions included urban-growth boundaries, purchases of regional parks and open spaces and various limits on building permits. These regulations created artificial land shortages that drove housing prices to extreme levels. Today, residents of Houston, Texas, can buy a brand-new four-bedroom, two-and-one-half bath home on a quarter-acre lot for less than $160,000. That same house would cost you more than five times as much in Marin or Contra Costa counties, seven times as much in Alameda County, and eight to nine times as much in Santa Clara, San Mateo, or San Francisco counties.

In fact, planning-induced housing shortages added $30 billion to the cost of homes that Bay Area homebuyers purchased in 2005. This dwarfs any benefits from land-use restrictions; after all, how livable is a place if you can't afford to live there?

The benefits of protecting open space are particularly questionable. The 2000 census found that nearly 95 percent of Californians live in cities and towns that occupy just 5 percent of its land. Many San Francisco Bay Area counties have permanently protected more acres as open space than they have made available for urban development. When such actions make it impossible for middle-class families, much less low-income families, to afford their own homes, they represent a sad distortion of social priorities.

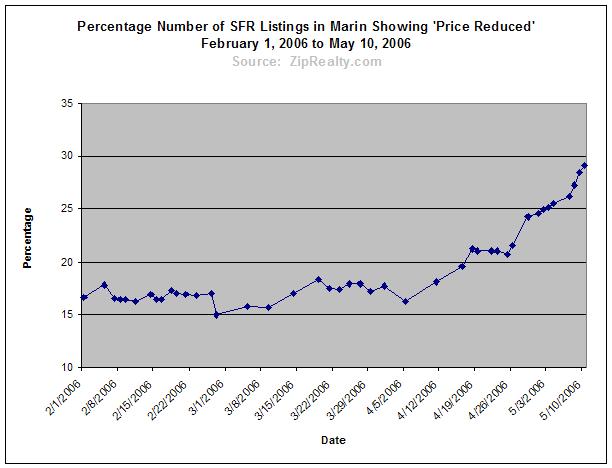

Moreover, as in the 1980s, California's fast-rising home prices have attracted speculators who have created huge bubbles in the state's housing markets. Bay Area prices fell by 10 percent in the early 1980s, 20 percent in the early 1990s, and are likely to fall even more as the bubble deflates in the next few years.

The impacts of high housing prices are also reverberating throughout the region's economy. First, economic growth has slowed as businesses look elsewhere to locate offices and factories. High housing costs have also increased prices for food and other consumer goods; retailers now pay $1 million per acre or more for store locations. Far from reducing driving as planners desire, high housing prices force many commuters to live farther away from their jobs, forcing more cars onto the roads. Ironically, an obsessive focus on protecting Bay Area "farmlands" (in fact, mostly marginal pasturelands) forces people to move inland and more rapidly develop the highly productive croplands in California's not-yet-so-unaffordable Central Valley.

The people most enthused about all these planning rules like to call themselves ''progressive.'' But the effects of planning on home prices are entirely regressive. Planning-induced housing shortages place enormous burdens on low-income families but create windfall profits for wealthy homeowners. Does this steal-from-the-poor, give-to-the-rich policy reflect the Bay Area's true attitudes?

Homeownership is more than just a dream, it is a vital part of America's economic mobility. Most small businesses get their original financing from a loan secured by the business owner's home. Children in low-income families who own their own homes do better on educational tests than those who live in rental housing. Barriers to home ownership reduce this mobility and help keep low-income people poor.

Predictably, planners' solutions to the housing affordability problem often make the problem worse. Planners typically require that homebuilders sell or rent 15 percent of their homes at below-market rates to low-income families. The homebuilders simply pass that cost on to the buyers of the other 85 percent of the homes they sell. Existing homeowners, seeing that new homes suddenly cost more, raise the price of their homes when they sell. The result: A few people benefit and everyone else pays more.

The solution to the Bay Area's housing affordability crisis is not a few units of affordable housing, but widespread land-use deregulation that will make housing more affordable for everyone.

{kind=link}