Thursday, January 31, 2008

War on Affordable Housing Bill

Here it is, the War on Affordable Housing bill that is currently in Congress (pdf).

Wednesday, January 30, 2008

Monday, January 28, 2008

They're BaaAAaack!

So I am skimming over the Ben Jones housing bubble blog and I notice the name "Marty Ummel" mentioned in one of the posts and I say to myself, "Hey, I know that name". I remember that name from a Marin IJ article that I almost chose to blog. I was unable to find the original IJ article in their archives (it was back in late 2005 or early 2006 if I remember correctly) but as I recall these were the folks who (for reasons that I find hard to believe) actually left God's Country (aka Marin County) for that "armpit" Southern California. As I recall they lived in the Dominican Hills area and Vernon and Marty Ummel were fund raisers for Dominican

So I am skimming over the Ben Jones housing bubble blog and I notice the name "Marty Ummel" mentioned in one of the posts and I say to myself, "Hey, I know that name". I remember that name from a Marin IJ article that I almost chose to blog. I was unable to find the original IJ article in their archives (it was back in late 2005 or early 2006 if I remember correctly) but as I recall these were the folks who (for reasons that I find hard to believe) actually left God's Country (aka Marin County) for that "armpit" Southern California. As I recall they lived in the Dominican Hills area and Vernon and Marty Ummel were fund raisers for Dominican Well, the Ummels are back in the news (you can see the video here). Apparently, the Ummels feel they paid too much for their SoCal house, they are watching it fall in value, and, naturally, are suing someone and that someone is their real estate agent:

CARLSBAD, Calif. - A North County woman who says she paid too much for her home, which she bought at the height of the housing boom, is taking her case to court.Now, don't get me wrong, I don't mind seeing the real estate industry being sued; I don't mind that at all. And I am sure there are a lot more law suits to come. But seriously, how many of you are actually going to tell me that the Ummels didn't buy with the full expectation that "houses only go up in price" and "now is [always] a good time to buy" so it doesn't matter if you willingly pay a stupid price for a house? These are former Marin residents after all and that makes them "special"; as the Marin RE bulls were frequently telling us "bubbleheads" early in the history of this blog, Marin residents are all rich, all financially savvy.

In 2005, Marty Ummel and her husband bought a four-bedroom house in Carlsbad for $1.2 million. The Ummels say their agent was dishonest about the price of other homes in the neighborhood, and then rushed them to close the deal before the Ummels found out comparable houses on the same street sold for as much as $175,000 less.

She has now filed suit against her real estate agent, claiming fraud.

""We feel that we were misled. We feel disappointed. We do feel angry," she said... We've worked hard and to think that we've done that our whole lives -- and then for a realtor not to tell us about the biggest purchase of our lives -- that there was a house selling for much less," she said.

But in a deposition, an expert witness hired by the defense said of the Ummels: "They simply didn't do what is expected of a knowledgeable sophisticated buyer, and are now looking for someone other than themselves to take responsibility.'"

The defendant in this case, Mike Little of Remax Associates, told the New York Times the case is quote "ridiculous."

"There are a lot of folks out there who are in a desperate situation right now with their homes and they're simply looking for someone to blame," said Diana Olick of CNBC.

"If they have information that is pertinent to their purchaser they should disclose it, but at the end of the day, the buyer is responsible for their own actions," said Robert DeLeonardis, the former president of the Manhattan Association of Realtors.

People in the real estate industry are calling this a "landmark lawsuit."

So what do you think? Do the Ummels have a legitimate gripe (listen to the reasons Marty Ummel lists in the video)? Is this case truly a "landmark" case? Will we be seeing more upside-down buyers suing their real estate agents? Or are the Ummels just more spoiled, whining Marinites who didn't get their way? And what does this portend for the future?

Saturday, January 26, 2008

On Raising the GSEs' Limits

“This would be absolutely, phenomenally excellent news for home buyers and sellers because it will help so many more people to qualify for loans that they can afford,” said Lori Staehling, president of the San Diego Association of Realtors.And the list goes on.* * *“Because the proposed change would make their houses more affordable to buyers, their houses might sell more quickly and for a higher price,” he [Matt Colonell, mortgage broker with Obispo Mortgage in San Luis Obispo] said.* * *NAR President Richard Gaylord, a RE/MAX broker in Long Beach, Calif., said that raising the loan limit on conventional financing is urgently needed. "The most effective way to stimulate housing and minimize the potential for a recession is for lawmakers to raise the limit on conforming mortgages to $625,000, which would open safe and affordable financing to buyers in high-cost areas," he said. "It is grossly unfair that some Americans do not have access to low-interest rate loans..."* * *The idea behind the higher limits is to stoke demand for homes in high-priced housing markets such as the East Bay and other parts of the Bay Area. "It will be as if interest rates are on sale. You could create urgency..." [said Vickie Nyland, president of the Bay Area division of Taylor Morrison, a homebuilder]* * *“Increasing the conforming loan limit will help homebuyers in the Los Angeles area at no cost to the taxpayer. If local banks can sell the loans they extend to Fannie Mae and Freddie Mac, the interest rates on those loans will be roughly ¼% lower.* * *The proposal would also allow buyers in the market, looking to finance a property with a loan of $729,950 or less, to make the purchase more affordable than it otherwise would have been under the current law.* * *Leslie Appleton-Young, chief economist for CAR, said decreases in the statewide median prices seen in recent months were the result of difficulties in obtaining jumbo loans.

[California governor] Schwarzenegger maintains that moderate- and low-income families in high-cost housing markets are "hit hardest" by the conforming loan limit, because it restricts their access to lower-cost, lower-down-payment, fixed-rate loans. "Lifting the GSE loan limit ... would help put affordable home purchase and refinancing options within their reach," the governor said...* * *The proposed new limit for mortgages with the most attractive interest rates would be, for costly markets such as the Bay Area...

"The changes would offer the stability needed to offer more home loan products," said Terry Francisco, a Bank of America spokesman. "If we and other lenders can offer more products, that will increase competition..."

So according to the real estate industry, the current "problem" with the housing market is a lack of affordable loans, not a lack of affordable house prices. As if a self-serving redefinition of affordability wasn't enough. We again need more "affordability products".

I cannot help but laugh at the depravity of the real estate industry and its political lackeys. So we are now back to the "affordability loan" thing. Clearly, the NAR, the CAR, and real estate agents have not learned a damn thing by the carnage they have helped to create all in the name of their 6% commission. Clearly, they have no qualms (moral or otherwise) about using the devastation currently being suffered by the hoards of "FBs" (which they helped to create) to push a feckless and foolhardy policy that they have been lusting after for many, many years; the real estate industry has no scruples over trying to re-inflate the housing bubble for just a little while longer even if it means extending the pool of FBs. Apparently, all that matters to them is the 6% commission; the people they claim to serve can all go to hell.

If this futile proposal to raise the conforming loan limit becomes law (and we all know it will be permanent) and when the inevitable backlash arrives, when the legion of FBs finally realize that the real estate industry's attempt to keep their dream of easy real estate riches alive was nothing more than a shameful attempt to continue to line their pockets at the expense of buyers for just a little longer, you, Mr. and Mrs. Real Estate Industry, will be "reminded" of your support. The collaborators will be named. The law suits will fly. A lot of eyes are watching, a lot of blogs are recording what you say and what you do. You can't hide. The tar and feathers are waiting for you.

Using people's current suffering to make a desperate, last minute, and short-sighted attempt at re-fueling unsustainable and unaffordable house prices via GSE loan limit increases is plain and simply wrong.

Do the right thing: Let the housing markets correct and heal themselves.

But then again, now that the NAR has gotten its way and Fannie Mae has changed its mission from helping poor and middle class families buy homes to helping mortgage bankers and lenders make money, why am I surprised? Sick. Just sick.

Thursday, January 24, 2008

Wednesday, January 23, 2008

"Just a Horrible, Normal Cycle"

Update 01/27/08: Added DataQuick's bar chart of defaults.

Well, by now you are probably all aware that DataQuick has their foreclosure data out for the Golden State. Needless to say, foreclosures for 2007Q4 are way up over 2006Q4. Here's DataQuick's chart of NODs:

Marin NODs are up 122% which is not the lowest for the Bay Area. That must be a mistake because we all know that Marin is immune, everyone here is rich and financially savvy, we are only two hours from skiing, and you can wear your shorts in the winter.

Marin NODs are up 122% which is not the lowest for the Bay Area. That must be a mistake because we all know that Marin is immune, everyone here is rich and financially savvy, we are only two hours from skiing, and you can wear your shorts in the winter.

And what's this? The increase in NODs for the Bay Area is greater than that "armpit", SoCal? Anathema! That must be a mistake too.

Here is what the Marin IJ had to say (emphasis mine):

And "just a horrible, normal cycle"? You're kidding, right? If you want to see just how horrible and not normal this cycle is, trek on over to Calculated Risk and feast your eyes upon this graphic. That aint normal.

And what are some home "owners" doing in response to the inevitable consequences of this horrible, not-so-normal cycle? Why, they are suing real estate agents of course. (Marin agents, take note.) Not that I think they are suing the right people. But when did Boobus Americanus ever think straight? All that Boobus knows is that he is angry and someone else has got to pay for his stupid financial decision making. That's the American Way after all.

And I found this article somehow relevant. I guess what caught my eye was the line “Many previously considered ‘prime’ customers who took on 80+% LTVs are performing closer to sub-prime loans” Are we getting primed for the Alt-A bomb?

There is nothing normal about this cycle.

Well, by now you are probably all aware that DataQuick has their foreclosure data out for the Golden State. Needless to say, foreclosures for 2007Q4 are way up over 2006Q4. Here's DataQuick's chart of NODs:

Marin NODs are up 122% which is not the lowest for the Bay Area. That must be a mistake because we all know that Marin is immune, everyone here is rich and financially savvy, we are only two hours from skiing, and you can wear your shorts in the winter.

Marin NODs are up 122% which is not the lowest for the Bay Area. That must be a mistake because we all know that Marin is immune, everyone here is rich and financially savvy, we are only two hours from skiing, and you can wear your shorts in the winter.And what's this? The increase in NODs for the Bay Area is greater than that "armpit", SoCal? Anathema! That must be a mistake too.

Here is what the Marin IJ had to say (emphasis mine):

Home foreclosures quadrupled in Marin in 2007, reaching record levels, and will continue to rise this year, it was reported Tuesday.And then:

Last year, a record 133 foreclosures were reported, up from 29 in 2006, according to La Jolla-based DataQuick Information Systems. Last year's total was the highest since DataQuick began tracking foreclosure figures in 1988.

The number of default notices issued - the beginning of the foreclosure process - climbed in 2007 to 632. In 1992, a record 645 notices were issued.

"It shows that Marin is not immune from these larger forces out there,"said DataQuick analyst Andrew LePage... "Marin has grown less than most counties, so it actually means a little more to be back at record levels," LePage said. "Counties like Contra Costa and Riverside have grown tremendously, so you would expect more."

In Marin, the median price peaked in June at $1.12 million but has dropped to $836,000.Did the IJ just say that prices are down 25% in Marin? Well, most of that is seasonal I suppose.

"I think even this county is being affected by the slowdown in the housing industry," said Jim Chapman of First Security Loan in San Rafael. "I'm not sure this isn't just a horrible, normal cycle."

And "just a horrible, normal cycle"? You're kidding, right? If you want to see just how horrible and not normal this cycle is, trek on over to Calculated Risk and feast your eyes upon this graphic. That aint normal.

And what are some home "owners" doing in response to the inevitable consequences of this horrible, not-so-normal cycle? Why, they are suing real estate agents of course. (Marin agents, take note.) Not that I think they are suing the right people. But when did Boobus Americanus ever think straight? All that Boobus knows is that he is angry and someone else has got to pay for his stupid financial decision making. That's the American Way after all.

And I found this article somehow relevant. I guess what caught my eye was the line “Many previously considered ‘prime’ customers who took on 80+% LTVs are performing closer to sub-prime loans” Are we getting primed for the Alt-A bomb?

The private mortgage insurance industry is under severe pressure from rising delinquencies and mounting losses. Now questions are swirling about how a potential blow-up in that sector will affect Fannie Mae.Remember back when people were justifying the housing bubble with "this time it's different", "we're special", "wealth creation technology", "financial dark matter", "fundamentals don't matter", etc? If any of that was true, if it wasn't just a ruse to disguise our own greed, then why are people losing their homes to foreclosure at an accelerating rate, why is the Fed in panic mode with an unprecedented 75 bp cut, why will the GSEs' conforming loan limits be raised to $650k, why is the Federal government going to mail out $600 checks to every tax paying citizen in the United States?

Fannie Mae… operates with the understanding that the insurers will pay it back. If one of these insurers takes a massive hit, then Fannie Mae’s underwriting standards may come under scrutiny, and the firm may be forced into buying fewer high-LTV mortgages in the future.

In a recent research note, CIBC analysts said the ‘highest losses will be driven by LTVs, not FICO scores.’ “Today, as a higher percentage of people own homes and many of them have taken on “too much house” or high LTV loans, things are different,” CIBC analyst Meredith Whitney wrote. “Many previously considered ‘prime’ customers who took on 80+% LTVs are performing closer to sub-prime loans.”

There is nothing normal about this cycle.

Sunday, January 20, 2008

Riddle Me This

Why is the real estate industry compensated for the value of the properties it sells and not the value of the service its agents provide?

Friday, January 18, 2008

Open Thread

So I was at a Marin middle school today. The teacher in one class was lecturing to a classroom of mostly 13-year-olds. The topic was global warming and its anticipated effects -- loss of habitat, changing weather patterns, flooding, extinction of polar bears and other creatures, human diaspora, famine, disease, etc.

So I was at a Marin middle school today. The teacher in one class was lecturing to a classroom of mostly 13-year-olds. The topic was global warming and its anticipated effects -- loss of habitat, changing weather patterns, flooding, extinction of polar bears and other creatures, human diaspora, famine, disease, etc.One of the students raised her hand and, after being called on, said "So your generation caused the problem and my generation has to deal with it?" The teacher was dumbstruck. God bless the honesty of children.

Needless to say my mind immediately started enumerating all the ways the generation currently in power has encouraged courses of action, laws, and policies that allow them to reap huge benefits/profits now, with little to no immediate cost to themselves, while passing the burden on to our children and our children's children.

How will the baby boomers be remembered?

This is my first "open thread". Talk about what you want.

Thursday, January 17, 2008

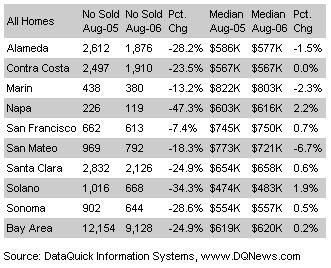

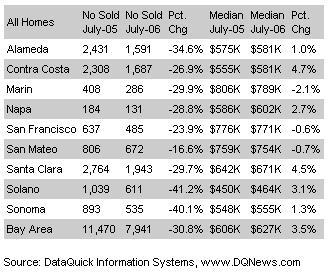

December, 2007

Ok, so I am going to break my self-imposed rule (ok, guideline really) and comment on DataQuick's latest because, well, frankly, it's been a while since we've seen negative price changes in Marin. And besides, judging by the off-topic meanderings of the comment thread in that last post, I desperately need an excuse for a new post...

According to DataQuick, it appears that Marin and SFO have joined the rest of the Bay Area with not just hefty sales declines, but price declines as well in December, 2007:

Now, we've seen negative price "appreciation" in Marin before from DataQuick (e.g., here, here, here, and here). So it is presumptuous to get worked up over this. If a pattern forms, well, then all bets are off of course. But I will note that this is the largest single month year-over-year decline in Marin prices from DataQuick that I've seen since I started paying attention to their data.

Now, we've seen negative price "appreciation" in Marin before from DataQuick (e.g., here, here, here, and here). So it is presumptuous to get worked up over this. If a pattern forms, well, then all bets are off of course. But I will note that this is the largest single month year-over-year decline in Marin prices from DataQuick that I've seen since I started paying attention to their data.

I found this quote from DataQuick's press release interesting (to say the least):

And then...

So what about sales? Below is a graph of the number of sales in Marin County for each month of December since 1994 (source: DataQuick archives):

Kinda reminds me of this:

Kinda reminds me of this:

So anyway, yes, that's right; December, 2007 Marin sales were the lowest they have ever been since DataQuick started collecting data.

Here is the historical view of the Marin Heat Index measuring sales activity (annotations are mine):

And what did the Marin IJ have to say... I don't care.

And what did the Marin IJ have to say... I don't care.

Ok, now it's your turn. What does it all mean? Or does it mean anything at all? Leave your comments at your leisure.

According to DataQuick, it appears that Marin and SFO have joined the rest of the Bay Area with not just hefty sales declines, but price declines as well in December, 2007:

Now, we've seen negative price "appreciation" in Marin before from DataQuick (e.g., here, here, here, and here). So it is presumptuous to get worked up over this. If a pattern forms, well, then all bets are off of course. But I will note that this is the largest single month year-over-year decline in Marin prices from DataQuick that I've seen since I started paying attention to their data.

Now, we've seen negative price "appreciation" in Marin before from DataQuick (e.g., here, here, here, and here). So it is presumptuous to get worked up over this. If a pattern forms, well, then all bets are off of course. But I will note that this is the largest single month year-over-year decline in Marin prices from DataQuick that I've seen since I started paying attention to their data.I found this quote from DataQuick's press release interesting (to say the least):

"There's been a significant drop-off in home financing with so-called "jumbo" mortgages. Because homes are expensive in the Bay Area, this has had a much greater effect on the market there. It looks like most non-essential buying and selling activity has been put on hold until things settle down," said Marshall Prentice, DataQuick president.Until things "settle down"? You're kidding, right?

And then...

The typical monthly mortgage payment that Bay Area buyers committed themselves to paying was $2,756 last month, down from $2,963 the previous month, and down from $2,828 a year ago. Adjusted for inflation, current payments are 5.5 percent above typical payments in the spring of 1989, the peak of the prior real estate cycle. They are 16.9 percent below the current cycle's peak in June last year.How can this be bad? People paying less, I mean. And the "typical" monthly payment is only 5.5% above that of Spring, 1989?! WTF is that? Eighteen years of (under reported) inflation and we are up only 5.5%?

Foreclosure activity is at record levels...You don't say?

So what about sales? Below is a graph of the number of sales in Marin County for each month of December since 1994 (source: DataQuick archives):

Kinda reminds me of this:

Kinda reminds me of this:

So anyway, yes, that's right; December, 2007 Marin sales were the lowest they have ever been since DataQuick started collecting data.

Here is the historical view of the Marin Heat Index measuring sales activity (annotations are mine):

And what did the Marin IJ have to say... I don't care.

And what did the Marin IJ have to say... I don't care.Ok, now it's your turn. What does it all mean? Or does it mean anything at all? Leave your comments at your leisure.

Friday, January 11, 2008

Sellers' Expectations

How true it is. And in Marin? Lots of sellers still asking, no expecting, no feeling entitled to prices from a year or two ago (emphasis mine):

How true it is. And in Marin? Lots of sellers still asking, no expecting, no feeling entitled to prices from a year or two ago (emphasis mine):During the recent boom, new housing got an even bigger price bump than existing ones because people often wanted the best, and, with a Icarian faith in the market’s eternal flight, buyers were willing to pay more and more to get the best. Now, with the downturn in the market, developers have scrambled to respond. The result? Some experts say that the price of a new house is now cheaper than an equivalent existing house.It was fairly clear as much as a year ago that the unwinding of the housing bubble would lead to recession. Never mind what the perma-bulls thought/said. Fast-forward to the present day: the housing bubble is unwinding around us and guess what? Merrill Lynch and Goldman Sachs are now on record as stating the obvious -- that we are heading to or maybe even currently in a recession. I guess not being an economist or paid to have a particular point of view is a good thing.

“I think that’s true," says Joseph Perkins, president and chief executive officer of the Home Builders Association of Northern California. "New housing is a better deal for prospective home buyers because builders are responsive to the marketplace, whereas some sellers still haven’t responded to the marketplace and they’re trying to sell their homes for prices from two years ago...”

So I ask you: Say you are a renter who is looking to buy a house in the Bay Area or maybe you are relocating to the Bay Area (my advice: turn around and go back), would it be wise to "buy" a Marin cottage which is asking a price from year or two ago (say, around $900k) realizing that you might lose your job in the foreseeable future? Or what about buying the median $650K house in the Bay Area? Or is it wiser to rent for 1/3-1/2 the cost of "owning" (not to mention the freedom to move easily from a rental in the event of job loss) and waiting? Or does the ingrained sense of RE entitlement that so plagues the Bay Area short-circuit any such financial reasoning?

And assuming a recession leads to a serious decline in the stock markets (seems like a sure bet to me, but what do I know?), will that lead to a disproportionate number of job losses in cities like SFO and NY where investment-related business is so prevalent?

So what's a seller to do? Pull the listing and hope it all goes away by next Spring?

Tuesday, January 08, 2008

Money For Nothing

I found this video over at the most excellent The Mess That Greenspan Made blog. Because the video has such great potential to educate and the blogger does not add anything new to the topic, I thought it was well worth cross-posting.

I found this video over at the most excellent The Mess That Greenspan Made blog. Because the video has such great potential to educate and the blogger does not add anything new to the topic, I thought it was well worth cross-posting.It is lengthy (about 50 minutes); the first few seconds are blank so be patient and wait for the video to start.

After watching it, you can then understand why it is that savers and restrained consumers are so despised (and punished) in America today.

And consider these quotes from the video and the power they imply for us peons:

"The people who actually produce all the real wealth in the world are in debt to those who merely lend out the money that represents the wealth."

"If there is no debt there'd be no money."

'If all debts were paid off, then there would be no money at all and it would destroy the financial system and the country.'

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Sunday, January 06, 2008

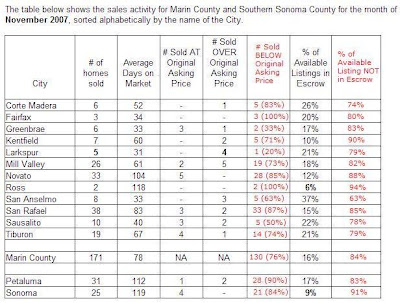

Some November, 2007 Data

The following is November, 2007 data that was sent to me by a Marin RE agent. I added the columns in red since for some reason that I cannot fathom they were missing from the original. I'm sure it was just an oversight on her part.

(Click on image for larger view)

(Click on image for larger view)

(Click on image for larger view)

(Click on image for larger view)Thursday, January 03, 2008

Awakening From My Slacker Slumber?

The Implode-o-Meter suit has been settled and has been dismissed. The last paragraph of the statement made by the Implode-o-Meter's author re-inspired me somewhat:

So I am not sure what to do with this blog. I've asked for help from readers but have received no commitments. I suppose I could shift gears and start focusing on the real estate industry itself as it is sorely in need of reform and frankly the NAR and its lobbying power should be outright destroyed. But perhaps they will self-reform (yeah, sure): One thing I found potentially inspiring was this statement from the owner of Marin's Vision RE newsletter:

So Vision RE is going to start reporting more realistic DOMs. If so, kudos to them. Is it possible that perhaps, just maybe, this and other similar blogs are having some effect? I mean I know I've ranted on more than one occasion about the bogus nature of the DOM statistic as commonly calculated. Can the real estate industry be reformed? It so badly needs it. One can only hope. Next stop for them is to make it clear that the bottom has fallen out here in Marin and current statistics are dominated by sales in the upper end. Furthermore, they should be making it clear that the paltry number of sales (140 or so in November, 2007) in Marin make the county statistics next to useless (and forget about being able to conclude anything based on statistics calculated for any individual town... yeah, only one house sold in Belvedere and it sold for $2 mill and Vision RE reports the town average/median is $2 mill? Give me a friggin' break already. See the problem folks? You cannot calculate meaningful statistics on a small sample size and expect to be able to generalize it to the entire population. You just can't. But that won't stop salesmen from trying).

But I digress...

Anyway, I turned comments back on so let me know what you think. Should this blog continue? What should we talk about? The bubble is old news now. Or has everyone given up on this blog in disgust with its blogger?

Because I am so very busy with work and family matters, I am more pressed for time now than I was before so please do not hesitate to email me content and let me know if you want to be acknowledged or not for said content.

PS - Please take note of the Terms of Use I added to the end of the page. I wrote it myself and because I am no lawyer I am not sure if it matters in a legal sense. If there are any lawyer readers out there who would be willing to write something better for me free-of-charge I would be most sincerely grateful.

We feel that the outcome of this suit represents only a partial victory for bloggers and internet-based public forums in general. The judge in our suit did agree that the site was indeed fundamentally focused on an important topic of public discourse. However, almost incomprehensibly to us, he did not dismiss the suit in line with the letter and intent of the CDA (section 230) and California's "anti-SLAPP" law. We strongly believe this was a grave mistake.

As is made clear by the costs we faced in the suit, providing a forum for whistleblowing and debate on critical contemporary issues remains a risky and expensive proposition. It is virtually "death upon challenge" for any individual or small-scale operation. It is thus unclear to us why anyone would ever get involved in such an enterprise if they truly understood the peril they were placing themselves in. We certainly would not have, if we knew then what we know now.

At a time when the internet's promise of lower communication barriers for average citizens is becoming a reality, the legal system remains the greatest threat to the public's receiving the benefit of this gift. Now, more than ever, we need to provide mechanisms which enable regular people to organize and fight back against entrenched corporate and government interests which have deeply corrupted our economy and society. This starts with, and relies centrally upon grassroots communication. So-called anti-SLAPP laws, such as California's law that we attempted to invoke, seem to be more of a fig leaf put out by these interests rather than a genuine attempt at reform. Sadly, this seems to be the state of affairs across the country, and the entire country is worse-off for it.

* * *

Someone over at the Sonoma Bubble blog left a comment that lamented my taking yet another break from blogging and stated that I have a responsibility to continue blogging. Responsibility? I beg to differ. But I understand the sentiment. The fact is that now that the housing bubble is widely recognized to have been just that, the bubble as manifested here and elsewhere has lost much of its interest for me. In fact, I've barley kept up with the news vis the housing bubble these last couple of months. This bubble blog was a lot more fun when the existence of the bubble was hotly debated.So I am not sure what to do with this blog. I've asked for help from readers but have received no commitments. I suppose I could shift gears and start focusing on the real estate industry itself as it is sorely in need of reform and frankly the NAR and its lobbying power should be outright destroyed. But perhaps they will self-reform (yeah, sure): One thing I found potentially inspiring was this statement from the owner of Marin's Vision RE newsletter:

I have not calculated the average days on market for this summary for one reason and one reason alone. The average days on market (DOM) per the Marin Multiple Listing Service (BAREIS) is NOT calculated correctly. It does not take into account a property that has been on the market with multiple brokers and those that have been removed for 30 days and then relisted. Once this is done it starts the days on market to ZERO. I will be doing an individual report on the actual DOM per community but it is very time intensive as the only way to accurately calculate the number is to look at the property history on each individual property. Since we have 659 single family homes on the market that will take a while. I promise to get you that information for the yearend report.You mean like these Marin POSs? That one shack in Mill Valley has been trying to sell since at least mid-December, 2005 (currently also trying to rent) but because these flippers (they first tried selling five months after purchasing) are unwilling to drop the price to what the market says its worth and instead are listing for what they owe on the dump, it can't sell and it doesn't rent and so they bleed cash month after month. Great Marin investment guys.

So Vision RE is going to start reporting more realistic DOMs. If so, kudos to them. Is it possible that perhaps, just maybe, this and other similar blogs are having some effect? I mean I know I've ranted on more than one occasion about the bogus nature of the DOM statistic as commonly calculated. Can the real estate industry be reformed? It so badly needs it. One can only hope. Next stop for them is to make it clear that the bottom has fallen out here in Marin and current statistics are dominated by sales in the upper end. Furthermore, they should be making it clear that the paltry number of sales (140 or so in November, 2007) in Marin make the county statistics next to useless (and forget about being able to conclude anything based on statistics calculated for any individual town... yeah, only one house sold in Belvedere and it sold for $2 mill and Vision RE reports the town average/median is $2 mill? Give me a friggin' break already. See the problem folks? You cannot calculate meaningful statistics on a small sample size and expect to be able to generalize it to the entire population. You just can't. But that won't stop salesmen from trying).

{kind=link}

But I digress...

Anyway, I turned comments back on so let me know what you think. Should this blog continue? What should we talk about? The bubble is old news now. Or has everyone given up on this blog in disgust with its blogger?

Because I am so very busy with work and family matters, I am more pressed for time now than I was before so please do not hesitate to email me content and let me know if you want to be acknowledged or not for said content.

PS - Please take note of the Terms of Use I added to the end of the page. I wrote it myself and because I am no lawyer I am not sure if it matters in a legal sense. If there are any lawyer readers out there who would be willing to write something better for me free-of-charge I would be most sincerely grateful.

Subscribe to:

Posts (Atom)