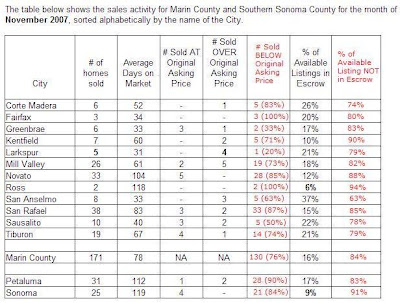

The following is November, 2007 data that was sent to me by a Marin RE agent. I added the columns in red since for some reason that I cannot fathom they were missing from the original. I'm sure it was just an oversight on her part.

(Click on image for larger view)

(Click on image for larger view)

(Click on image for larger view)

22 comments:

Marinite.. thanks for all your work and the extra data fields on this s-sheet.. of course, a lot of this data is highly suspect to me.. esp "days on the market".. we all know the games played behind that stat..

I have no doubt that, through this period of price correction, houses in Marin and elsewhere will still be sold for asking price or higher now and then.. home buying is still as much of an emotional decision as anything and not necessarily just a mathematical or financial decision.. and yes, there is also a lot of money in Marin, so getting the best deal possible is not that important to a number of people around here..

I'm not one of them, and will stick with the math and my gut.

Wow. So 75%+ of available inventory isn't in escrow. Lots of sellers in denial, I suppose. The few people who are buying may well fall into Matthew's description. Plus, a lot of buyers in Marin have families, and for some reason, people think if they have kids, they need to own or continue to own.

2003 Alt A loans will start to reset this year, and 2004 will reset next. I know Marin thinks it's "dodged the bullet", but we'll just get hit later in the cycle.

When will people realize that unless you're in a period of rapid appreciation, it makes ZERO sense to pay more to own than to rent??!!

I have no doubt that, through this period of price correction, houses in Marin and elsewhere will still be sold for asking price or higher now and then..

Furthermore, sellers can ask anything they want. They might ask for way more than they expect to get so that they can offer a "discount" later. Or, they can ask for what the market says its worth in which case the % in escrow would be higher and the "selling at asking" number would be higher. So these data don't mean much but can easily be spun which is no doubt why realtors like to make a big hoopla about them.

Having made that qualification, I think the data indicate that 84% of Marin is still in denial.

Oh, and yes, no one should doubt that I think the DOM statistics listed here are BS.

I read this article by Paulson below and want to barf.. sorry, I do.. I cannot help but to recall Sir Alan's remarks that the Fed cannot predict a bubble from forming nor should it be their job to prevent them.. BS.. maybe so with soybeans, gold and corn, but housing is different..

Housing was treated as a commodity and now that commodity is undergoing a long over-due correction.. it's too bad that millions of Americans have their financial futures and family's safety and health tied to this commodity.. it's waaaaay too bad that housing has dominated American's consumption habits over the last 6 or so years.. first through HELOCs and now through a neg savings rates brought on manily due to the excessive costs of this basic human need.. not much money left over for other discretionay things..

The Fed saw all of this forming and did nothing while the pigs on Wall Street and NAR lined their pockets from the lucrative bond market.. now the pain (or hangover) is starting and our leaders / saviors are on it..

Sorry, you're 5 years too late.. Deal with it.. but leave the tax payers alone.. we're stretched enough as it is, esp w/$100 oil and healthcare, college costs rising...

http://biz.yahoo.com/ap/080107/paulson_housing.html

I think this year's resets all the way to 2011 will tell us who all has been swimmin' nekkid' in Marin and Sonoma County. Our press keeps trotting out "we didn't have much subprime here so we are going to be fine and prices will rebound soon" and riding it all over the place. Soon it is going to be the dead horse of yet another "its different here" lie the FBs like to tell themselves.

You would think some would catch on that "we didn't have much subprime here" wouldn't actually help their delusion.

We didn't NEED to have a lot of subprime foolishness... We had a TON of GREATEST Fool Prime and Alt-A borrowers. We don't NEED no stinkin' subprimers, and our meltdown will make the subprime debacle look trivial.

"We didn't NEED to have a lot of subprime foolishness... We had a TON of GREATEST Fool Prime and Alt-A borrowers. We don't NEED no stinkin' subprimers, and our meltdown will make the subprime debacle look trivial."

Amen. And think of the higher price point of the homes purchased with Prime or Alt A loans versus Subprime. I live in San Anselmo, and little cottages went as high as $900K during the bubble. What happens when those loans reset?

Marin really seems to think that because we've escaped the subprime bomb, we'll be just fine, thank you very much.

My understanding is that piggy-back loans have pretty much disappeared, which is probably why the lower end has dried up. Who has 10% or 20% saved up?? At these prices?? Yeah right.

Yep, Lisa. The higher price points are precisely what is going to yank the tide out on the nekkid swimmers. Sonoma County's prices TRIPLED from 2000-2005. A lot of buyers took on bigger loans than they could afford. Many of them were not looking for long term housing. They were told that nobody pays off a loan anymore, and housing only goes up, and due to their good credit they could get this loan for 5-7 years that would allow them to have low payments and then sell. They were sold on the statistics that homeowners don't stay in their houses much longer than 5-7 years and they thought they would be fine.

Now their loans will be resetting and they will be faced with figuring out how to continue paying on their loans. Tsk, Tsk, Tsk... we will find out just exactly who had great credit, but no sense.

We don't need no stinkin' subprime here. We got all the foolishness stored up for the rainy days ahead. While other areas that didn't have such fortunate fools with great credit in their demographics bottom out and eventually stabilize... our show will just be getting started. Keep the popcorn handy and be sure to grab a comfy chair.

I live in San Anselmo, and little cottages went as high as $900K during the bubble. What happens when those loans reset?

...

My understanding is that piggy-back loans have pretty much disappeared, which is probably why the lower end has dried up. Who has 10% or 20% saved up?? At these prices?? Yeah right.

Of those people who can afford to make a 20% downpayment and are now required to do so, who would buy a cottage at $900k? That is precisely why my favorite POS in Tam Junction (by now you should know the one I refer to) and most if not all Marin POSs like it cannot sell and has not for the last two years despite their desperate attempts at doing so. If people really believed that "prices can only go up" then that POS would have sold in a heart beat.

So what's the first really ugly year for Marin and Sonoma? 2008? 2009? When will folks understand that we're NOT "different" here?

Lisa,

If I had to lay a bet, it would be that reality won't really hit full in the face for Marin and Sonoma County until sometime in 2009, possibly into 2010.

My reasoning is that the 2008 resets may not topple the Alt-A and Primes immediately. Depending on the price they paid, the ultimate reset, their ability to refinance to feed the alligator for a while, dip into savings, and liquidate other assets or perhaps send a spouse to work that had been staying at home due to HELOC $$ to try to hold on, it will be sticky slide down.

There will be big numbers of resets in 2008, but some may hold on for a while as their albatross gets heavier and heavier.

Initially the blame will still be on those subprimers who peed in the koolaid. Those who are the first to go under because their reserves run out and no greater fool turns up to catch their falling knife will blame the subprime meltdown for "qualified buyers" not being able to get financing.

But many will lose their grip, and when they do, their house will be thrown on the pile of foreclosures stacking up. As those stack up, the banks will eventually start getting serious about unloading them and tanking the comps for the FBs.

2009 will have more resets, and by then the market will be even more decimated, and likely the foreclosed properties that are in firesale territory will be what sells, and the FBs will find they are competing with Builders, foreclosures and owners with enough equity from long term ownership to price competitively, and other FBs like themselves.

We will know when the realization has kicked in when people start to ask how this could happen and the word on main st. Sonoma County and Marin was that people simply bought houses they couldn't afford.

THEN the wake up call will have been received. What happens then? Not sure... but this is how I am betting it plays out. We are real slow on the uptake and even though people around here are acknowledging behind closed doors that people bought $hit they couldn't afford... they still say.. it is different here, there is a lot of money here, everyone wants to live here. they content themselves that just the posers and those last buyers who took out subprime are cause for all the ruckus. They aren't convinced that the % of posers might be real close to the # of buyers.

Even though the data is out there, and the mainstream media has picked up the torch of the crash of the housing bubble, Sonoma and Marin still thinks Wall St. and the media are talking about everyone else.

Our show is still selling popcorn and organizing the seating... the trailers aren't even showing yet. Stay tuned though... ;-)

"We are real slow on the uptake and even though people around here are acknowledging behind closed doors that people bought $hit they couldn't afford... they still say.. it is different here, there is a lot of money here, everyone wants to live here."

And they are counting on a GF to buy their albatross and bail them out of their decision to buy a house they couldn't afford. But if sales stay in the crapper, and it becomes accepted that liar loans are out and 20% down payments are in for Jumbo mortgages, then folks may start to realize what a nightmare "investment" RE has become.

And given all the MSM coverage of Subprime folks not able to afford their resets, I am thinking Alt A and Prime may start to crumble before those loans actually re-set. If the writing is on the wall, you know you can't afford the re-set, why bother hanging on? And given how incredibly expensive it is to live here, how long will folks be able to hang on?

Let's recap the Real Estate Industry's contribution to society, shall we...

1. Unprecedented debt levels across the country.

2. Unprecedented foreclosures across the country

3. Largest transfer of wealth in our nation's history from the working class to the elite Wall Street bankers (or thugs).

4. Family values flipped from education and hard work to boob jobs and get rich quickies.

5. Tent cities forming on the outskirts of southern cities (a new favorite RE machine contribution of mine).

6. New educational TV shows abounding, with flip this and sell that house and, oh yes, that OC wives beauty of a show (very much a RE machine outgrowth IMO).

7. The desolation and eventual total destruction of neighborhoods in many industrial manufacturing suburbs.

I've got to run, but feel free to add your own...

Sorry, had to jot one more thought before heading off this morning which came to me after reading Paulson's most recent comments on the economy..

As a country, we got what we asked for (or allowed), that's for sure.. My list above and all the other pain we'll endure for many years is what happens when we allow Wall Street to lock horns with Main street. Paulson is guilty up to his ears in helping create this mess and Goldman-Sachs and he profited incredibly from all of it for many years. Now, he's our savior to help remove all the excesses... just amazing..

I've read a number of articles recently on how these same WS bankers have duped city and state pension fund managers to take mortgages/CDOs etc off their books (eg Jeb Bushy in FLA) in order to pass the losses onto the hard working people in those states and cities... just amazing..

Mathew,

I haven't been following Paulson's statements closely enough (and I don't think any other bloggers have either) like I did for Lereah. So...

Put together an incriminating statement/article against Pauslon (with quotes and reference hyperlinks of course), and send it in as a post to this blog. You will be doing readers a service.

I am involved in a "rocket science" project at work (and at home) for the next 6 months to a year and so find it difficult to find the time.

By the way, I heard on NPR this morning a discussion about raising money for education and they had someone on who represented the California community college system. The Community college rep made a comment that enrollment is booming in the Community college system as real estate agents and construction workers seek retraining.

I wholeheartedly agree with the hilarious prices for the complete PoS's offered up in Sausalito, Mill Valley, Tiburon. But what's the answer? We sold our house in SF because the neighborhood was heading south fast, and we were tired of SF stink and attitude, etc. I guess we're falling into a cliche at this point wanting a little fresh air, somewhat of a view (we don't have kiddos so school areas aren't a problem). If we don't re-purchase, we'll get completely reamed by taxes (no we're not rich, but USGovt doesn't take into account the cost of living so we fall into AMT), plus if we wait too long, we'll get priced out of the market, as we only have a little for the downpayment.

What is the general consensus of your readers and yourself if you need to buy in this inflated market?

Glass half empty or full...

Percentage sold below list price and percentage NOT in escrow - the marin real estate glass looks half empty to me!

Glass is broken..

"If we don't re-purchase, we'll get completely reamed by taxes . . . "

How so? Whether you re-purchase or not, I don't see how this impacts your tax situation. You get the $250,000/$500,000 capital gains break whether you buy again or not.

Glass is just twice as big as necessary. Not surprising in Marin, the home of the pseudo socially conscious trustafarian hypocrite.

Happily, it looks like the SFH rental market in Marin is starting to break loose, finally. At long last there is a supply of 3BR+ homes for rent at market instead of at "please cover my PITI".

House down the street has been on the market for some time. Checked into an open house yesterday. The house has been in and out of escrow once at 770k and another at 752k. Now it is at 745k. I wonder how many of the houses in escrow are actually going to sale.

Post a Comment