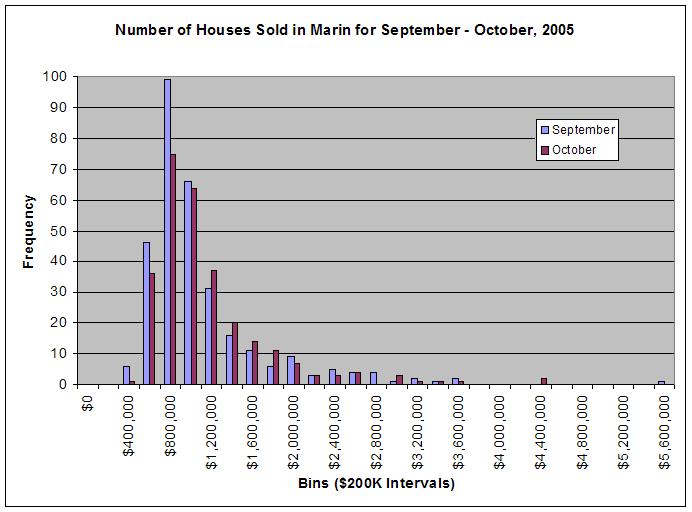

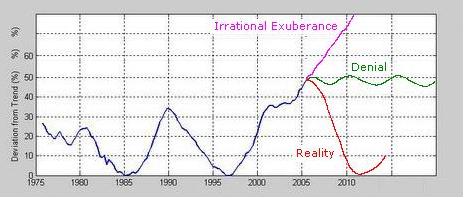

Look at these charts from Investor's Business Daily; especially that middle one; supply is dwindling until we hit 2005 and then it rockets up.

Look at these charts from Investor's Business Daily; especially that middle one; supply is dwindling until we hit 2005 and then it rockets up.Some choice quotes:

"Fall chills hit existing-home sales in October, even as prices kept climbing. It's the latest of several signs that the housing boom is finally over."

"Existing-home sales fell 2.7% to an annual rate of 7.09 million from Sept.'s revised 7.29 million, despite heavy selling in areas hit by Hurricane Katrina, the National Association of Realtors said. Without storm-related sales, the drop would have been 3.2%. The number of unsold homes hit a 19-year high of 2.87 million — 16.3% higher than a year ago."

"In what many analysts see as some last-gasp gains, home prices continue to set records...the median sales price in October was [up] 16.6% above a year ago. Such huge advances are not sustainable, economists say."

"...high-end home prices are already cooling. The rest of the market is expected to follow, since higher prices can't hold up as sales fall and supply swells."

"In red-hot markets like Florida and California, sellers appear to be losing their grip on the market..."

"In California, real estate agents saw sales drop 2.8% vs. a year earlier while prices fell 1% from September. But the median price for a single-family home still swelled 17.2% vs. a year earlier to an eye-opening $538,770."

"...foreclosures and defaults are starting to pick up. U.S. foreclosures jumped more than 18% in October from September, according to Web foreclosure marketplace RealtyTrac. Another report from Foreclosures.com showed rising mortgage defaults in California too."

{kind=link}

{kind=link}