The Marin IJ (Marin's main local paper) has published their response to DataQuick's May, 2006 report on Bay Area real estate. Naturally, the IJ, beholden to their RE masters, has of course put the most positive spin they could on it:

The Marin IJ (Marin's main local paper) has published their response to DataQuick's May, 2006 report on Bay Area real estate. Naturally, the IJ, beholden to their RE masters, has of course put the most positive spin they could on it:The median price for single-family homes, not including condominiums, dropped about 8 percent from $979,000 in April."It is too soon to see whether this is a trend that will continue for the year." True enough as a trend can never be positively identified until after the fact (when no one, except historians, really cares anymore). But I don't believe a word of it and I don't think you should either. I cannot foresee the future any better than you of course, but I do have records of past market behavior at my disposal to inform my decision-making process. Below you will find some charts I made and put up on this blog quite some time ago.

Kathy Schlegel, president of the Marin Association of Realtors, said several factors drove the median price down last month.

"Inventory has increased and more homes are staying on the market longer, so it has become more competitive," Schlegel said. "Buyers and sellers are negotiating prices down. When we have all that working together, it will tug the prices down."

Schlegel, an associate broker with LVP Marin, said the figures reflect a return to a normal market.

"It goes up and down throughout the year, so if you look at the year it balances out the increases and decreases in price," Schlegel said. "We are back to seeing more negotiating between buyers and sellers, which is healthy for a more balanced market."

Valerie Castellana, an agent with Pacific Union and association president-elect, said it was still too early to know whether a trend is taking shape.

"The changes from April to May in 2006 are a snapshot in time. It is too soon to see whether this is a trend that will continue for the year," Castellana said. "Reality may be setting into the market. We have been on a roller coaster ride and now it is more of a teeter-totter with buyers on one side, sellers on the other and statistics moving around month to month."

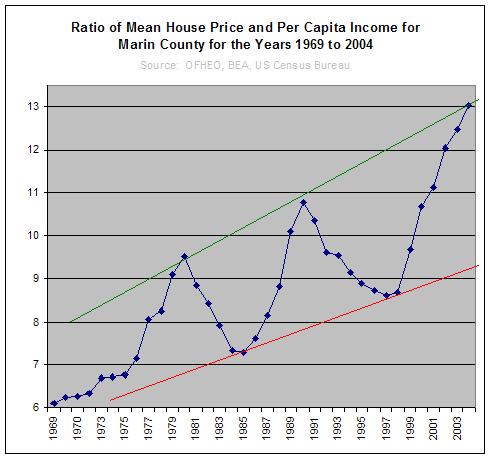

The following chart can be found here; it shows the ratio of mean Marin SFR price to per capita income. If you project the trend line into the future and assume that income increases only a few percent a year (as it has been), then we are looking at about a 25-30% drop in SFR price relative to income over the next few years:

The following charts can be found here; the first one shows the same sort of data as the previous graph and makes a similar prediction:

The next two charts show that Marin's SFR prices are greater than two standard deviations away from the mean. The reason why this is significant is that researchers have found that for every single financial bubble that they investigated where prices have increased by two or more standard deviations away from the mean, prices have reverted back to the mean. Please re-visit the original post to get more detailed information:

Unless you believe that incomes will increase at a fantastic rate over the next few years, history is telling us that we can expect Marin SFR prices to revert to the mean which implies at least a 25-40% drop in prices.

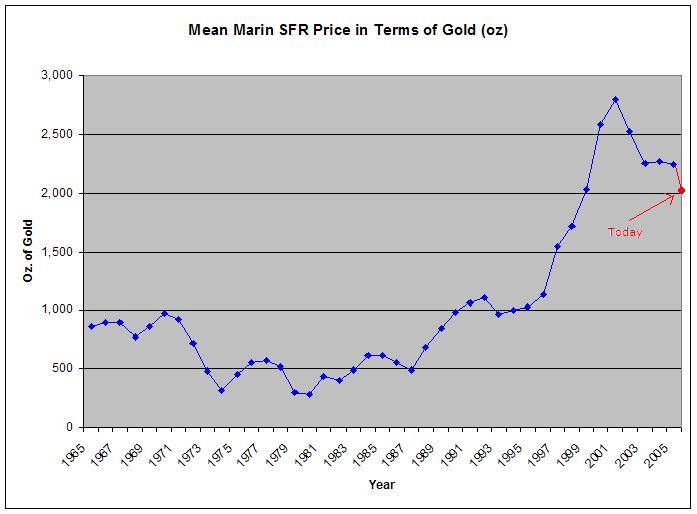

Lastly, there is this chart which shows Marin SFR prices expressed in terms of ounces of gold (thus nicely taking inflation into account):

Now add in the facts that mortgage rates are going higher which is far more likely to continue than not, foreclosures are rising at an alarming rate, adjustable rate mortgages are starting to reset and will only get worse, faudulent appraisals and lending is starting to be closely examined, and loose lending standards in general are being tightened.

Now add in the facts that mortgage rates are going higher which is far more likely to continue than not, foreclosures are rising at an alarming rate, adjustable rate mortgages are starting to reset and will only get worse, faudulent appraisals and lending is starting to be closely examined, and loose lending standards in general are being tightened.I don't know about you but I am not terribly optimistic.

6 comments:

we can expect Marin SFR prices to revert to the mean which implies at least a 25-40% drop in prices.

And, judging by the magnitude of this recent runup, can we safely predict a longer and deeper reversion than any previous boom? Marin houses may drop, but I think it may take some time.

explorer -

Yes, it will take time.

marinite -

You are the man.

I love all those charts.

Just absolutely love them.

There is not a better way to show the stupidity we've been through.

I mean, MFG, I thought I'd "seen it all" from ground zero durinig the dotbomb in SF, with all the funny money squirting all over the place due to the venture idiots, the IPO's of crap companies and AG and such... and then later drying up.

Well... mostly drying up (from that, anyway).

And now I get to see another market changing event in a similar way once again in my lifetime.

Albeit, likely to be a "slower" one.

And would the IJ dare to show even one of those charts?

Just one?

Love the charts but remember that the bottom points hint at the most conservative credit of the cycle--and credit has become generally looser over the last 30 years (each bottom is higher than the last). I'm not sure if the upward slope is an artifact of the national/international general credit market or how much more credit people can absorb. The next bottom may match or be lower than the last bottom.

If credit became tighter than it has been in 30 years prices would fall substantially below the trendlines. I'm not counting on that, however.

I am expecting an eventual realization in other countries that they can sell to each other rather finance US debt, and the subsequent loss of our EZ money.

marin_explorer: it's a credit bubble not a housing bubble. If the loan money dries up prices might fluctuate dramatically or crash. If credit remains "near normal" then expect a long slow Japan-style decline.

"it's a credit bubble not a housing bubble."

Yes--some of my colleages were already warning of this during the dot-com boom. That said, there's still a bit of psychology behind housing in some markets, such as Marin. I tend to think there's only so much liquidity left to keep sales volume going, so perhaps even Marin could feel pain? Perhaps it's already started.

Marinite-

I think the best vindication re: the IJ is the data you provide here.

"it's a credit bubble not a housing bubble."

I find it helps to think of the "credit bubble" (plus lenders, appraisers, etc) as being 'the enabler' and people and their manic psychology as being 'the actor'.

I think the best vindication re: the IJ is the data you provide here.

Data always speaks loudly. The Marin IJ has engaged in ceaseless spin and they are the local RE industry's poodle. In the past I have caught them in the act of selectively using data to promote the story they want people to believe. In one case that I remember about a year ago they took some official data that said sales in the Western Region were up something like 7% (as I recall) and the IJ reported it as if that figure was for Marin. I wish I had started this blog then as there would be a public record of it. But alas, the thought of writing a blog had not occurred to me by then.

If we all write them angry letters insisting that they start covering the situation more objectively, in a more balanced fashion, then, if they do, we are all (we Marinites anyway) better off IMO.

Post a Comment