Saturday, September 30, 2006

The End of "Liar Loans"?

Well, this will crimp the Bay Area house buyer's style -- lenders will be able to easily verify potential borrower's income in a couple of days over the internet. Hopefully, we'll be able to say goodbye to "liar loans" which have been helping to prop up Bay Area prices. This is potentially big news. But as I am a little late in the game on this one and since my esteemed fellow blogger up in Seattle has done a much better job of discussing it than I could, I will refer you to that blogger's discussion -- "The Mother of All Weekend News".

A Quote From La-La Land

“So I guess it’s official: The real estate market is tanking... If you’re a renter, you now have permission to be as self-satisfied as the homeowners who once taunted you with their dizzying appreciation rates. As for us owners, we can just cover our ears and sing ‘Correction! Correction! I can’t hear you!’ until things start looking up again. Call it a correction or call it a crash. Either way, the party’s over.”

“So I guess it’s official: The real estate market is tanking... If you’re a renter, you now have permission to be as self-satisfied as the homeowners who once taunted you with their dizzying appreciation rates. As for us owners, we can just cover our ears and sing ‘Correction! Correction! I can’t hear you!’ until things start looking up again. Call it a correction or call it a crash. Either way, the party’s over.”That's what they're saying in the LA area. Well, it's an "armpit", right? At least it can't happen here. I'm so relieved.

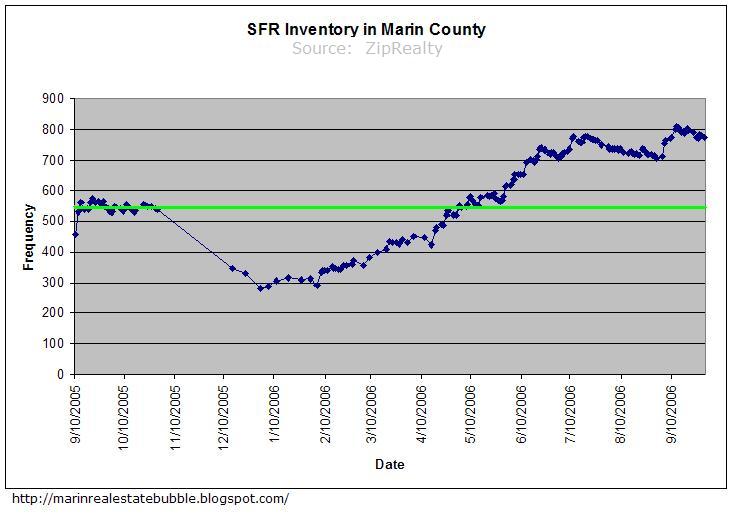

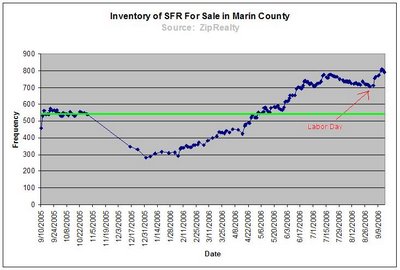

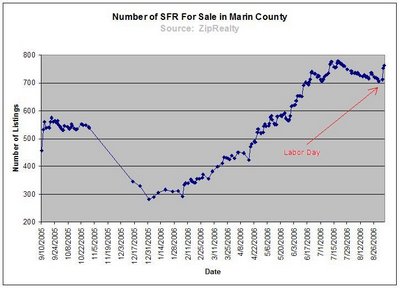

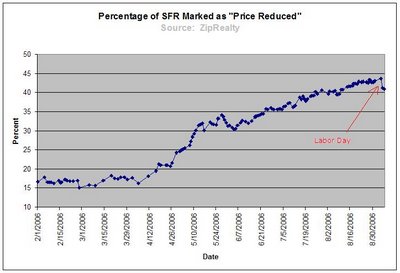

That recent drop in the above graph is due to the rapid increase in inventory following Labor Day. I'm glad to see the trend continuing on schedule (it takes sellers some time before they can admit to needing a price reduction even if it is superficial).

That recent drop in the above graph is due to the rapid increase in inventory following Labor Day. I'm glad to see the trend continuing on schedule (it takes sellers some time before they can admit to needing a price reduction even if it is superficial).

Thursday, September 28, 2006

Quote of the Day

"Bubbles are belief systems. You cannot reason a person out of a belief that they did not arrive at by reason, particularly if that person has money, reputation, or employment – or all three – that depend on dot com or telecoms stocks, or housing, or dollar denominated assets, or all three. A man or woman with everything on Number Seven has got to believe that Seven is their lucky number. Or that they are not betting, they are investing in a New Era."

Source.

Source.

Wednesday, September 27, 2006

Confidence Intervals and the USDUD's Data

The folks over at Patrick.net have it right about the correct interpretation of the latest US Department of Urban Development statistics (PDF) on new home sales... the confidence intervals around their latest figures are so huge as to make the results statistically meaningless. And how much do you want to bet the numbers will be revised down next month as, lately, they almost always are?

The folks over at Patrick.net have it right about the correct interpretation of the latest US Department of Urban Development statistics (PDF) on new home sales... the confidence intervals around their latest figures are so huge as to make the results statistically meaningless. And how much do you want to bet the numbers will be revised down next month as, lately, they almost always are?What is a confidence interval? Well, you could read all the mathematical gibberish by going here or you could just think of it this way:

If someone says, for example:

"The average percent change in new housing sales for August for the entire Western region of the US was down a -17%"What they are really saying is:

"It is, for all practical matters, impossible for us to measure every housing market in the entire Western region of the US and so we must measure a representative sample of markets. By 'representative' we mean that we believe this smaller sample of the overall market is a valid reflection of the entire, overall Western US housing market. Given the results from our sample, we claim that the average for the entire, overall Western US housing market is down a -17%".If they then tell you that the 90% confidence interval for their measure is, say, 13% what they mean is:

"There is a 90% probability that the true average for the entire, overall Western US housing market (as opposed to just our sample which no one really gives a hoot about) falls somewhere within -17% plus-or-minus 13% or, in other words, somewhere between -30% and -4%; there is a 10% chance that the true average for the overall Western US housing market is somewhere outside this range."The larger the confidence interval, the more uncertain you should be that the reported average accurately reflects the true average for the entire population (the Western US housing market in this case). E.g., if the confidence interval had been just plus-or-minus 1%, then the claim would be that there is a 90% chance that the true average for the entire Western US housing market falls somewhere between -18% and -16%.

A confidence interval is not restricted to 90%; 95% and 99% are more common and of course reflect greater degrees of certainty. If the USDUD had chosen to use the 95% confidence interval, then the interval range would have been even larger which is probably why they went with the 90% confidence interval which is the lowest confidence interval that still retains a shred of credibility.

Ok, I've done my good deed for the day.

Update: “In the West, prices have held steady there this summer, sales have fallen. ‘Something’s going to give in the West,’ Mr. Lereah said. ‘The correction has not occurred in the West yet. Sellers are stubborn there.’”

Tuesday, September 26, 2006

Paying Boardwalk Prices for Baltic Avenue

Q: Why is the cost of housing so much more in the Bay Area than pretty much anywhere else?

Q: Why is the cost of housing so much more in the Bay Area than pretty much anywhere else?A: Because the Bay Area is the bestest place in the whole world, that's why.

Q: Why is it claimed that everyone here is rich or at least pulling down a fat stack of income?

A: It must be true...just look at the prices everyone pays for their crappy POS of a house.

I don't know exactly what originally caused the Bay Area's housing markets to go down the path they did..some twisted combination of NIMBY land use policies, Prop 13, building regulations up the wazoo, etc. But I have to wonder if the prevalence of "stated income" loans (aka "liar loans") in the Bay Area doesn't have something to do with it too. People can seemingly afford to pay our ludicrous housing prices and appear to be making bookoo dollars by virtue of being able to claim whatever income they want on a loan. And all too often, the buyer doesn't even know that their income is being inflated!

It's like:

Lender: "That $500K loan for that 1 br 1 ba, 600 sq ft Marin tear-down will run you $4000/month."Check out the video at the end of this link and/or read the transcript (thanks to a reader for the link).

Buyer: "But I can't pay that much each month because my income is only $3000/month."

Lender: "Don't worry about it; I'll take care of everything. Your monthly payment will be $2800. Just don't read the fine print."

Buyer: "Uh, ok."

This quote from the video -- "We've seen the banking industry keep getting more creative, and more creative, and more creative to keep putting fuel on this fire of home appreciation" -- makes one think what happens when the fire goes out? What happens to Bay Area house prices when you can no longer lie on your loan?

And if it does come to a stop sooner rather than later, do you really want to be buying now? Is now really a good time to be paying top dollar/speculator pricing for a Bay Area house?

Here are selected excerpts from the transcript (emphasis mine):

What if you could get into Stanford by simply telling the admissions office you are an A-plus student -- without any proof? Or how about driving a brand new Mercedes off the lot after promising the salesman you'll send him a check next week? Fat chance, right? So you might be surprised how easy it is for people buying a new house to borrow hundreds of thousands of dollars by simply telling the bank how much money they make -- without any proof. It's called a "stated income" loan, but many people inside the housing industry call it something else: a "liar loan."What happens when investors finally wisen up and say "we're not going to buy your junk debt any longer"? Interest rates go through the roof, that's what.

Brian is a Bay Area mortgage broker. "Michael" is his client -- a 23-year-old auto mechanic. The payment on Michael’s new home is $4,200 a month, but he only earns about $4,000 a month -- leaving him $200 in the red. He was only able to get the loan because his broker used "stated income" to inflate his paycheck. Brian (the broker) said, "I put on the application that he made $13,000 a month, which was unverified … That's the definition of a stated income loan. You state the income. Most definitely it was a fraudulent loan. The income was literally made up from thin air."

Last May, Beverly and Dwayne [Bay Area residents] bought their first home. Their broker assured them they could afford the half-a-million-dollar price tag based on Beverly's income as a social worker. She makes $2,750 a month. But what they didn't know? To make the deal work, the broker boosted Dwayne's salary to an impressive $8,000 a month. "Right now I'm living from paycheck to paycheck. I'm struggling with putting gas in my car just to get to work," Beverly said. "I wish I did make $8,000 a month," Dwayne said. In truth, Dwayne is out of work and only gets a small disability check. Nevertheless, based on their inflated income, they qualified for a mortgage of $3,700 a month. That's almost $1,000 more than Beverly's entire paycheck.

...over the last decade, Bay Area home prices have gone up 300 percent -- far outpacing people's incomes -- which is why nine out of 10 households can no longer afford the median home price of $630,000. So to keep the clients and cash rolling in, banks and other mortgage companies began offering easier terms like no money down, adjustable rates, interest-only, and stated income.

One broker, "Dennis," works for a mortgage company where he says a whopping 85 percent of loans are stated income. He says out of that 85 percent, they all have inflated numbers. Dennis added. "We've seen the banking industry keep getting more creative, and more creative, and more creative to keep putting fuel on this fire of home appreciation."

But the buyers may not even know their incomes are being inflated. Dennis said, "Some may know. But for the most part I would say the consumer is pretty much left out of the loop." Out of the loop because the broker often prepares the loan papers without ever telling the buyer their income has been inflated.

Now you might think mortgage lenders would be more careful giving out hundreds of thousands of dollars without proof of income. But in fact there's almost no risk to the bank. That's because most banks turn right around and sell their loans to real estate investors on Wall Street -- to mutual funds, pension funds -- even foreign countries. "In today's environment, if a family does not repay [their loan], some nameless, faceless guy in Wall Street in New York, or the investors take the hit. The bank is not put at risk at all, and so they're not that concerned."

Beverly said, "You know they say you make sacrifices to keep what you have, but they didn't tell me I would totally have to stop living and just exist because of somebody else's deceit."

Oh No

It's old news now and it's not specific to Marin, but I couldn't resist this article in USA Today if for no other reason than Lereah's comments at the end:

It's old news now and it's not specific to Marin, but I couldn't resist this article in USA Today if for no other reason than Lereah's comments at the end:Home prices are projected to fall for the rest of the year, the National Association of Realtors said Monday, with sellers being forced to accept a new reality: Buyers now wield the power, with the supply of homes for sale at a 13-year high.A nation-wide price drop is truly noteworthy.

The median-priced U.S. single-family detached home... fell 1.7% in August to $225,700, compared with a year ago. The decline is no doubt jarring to sellers, who haven't seen prices fall nationally since April 1995. The price drop was also sharp, the second-steepest in 38 years.

"The housing bubble has burst; this is just the confirmation," says Joel Naroff of Naroff Economic Advisors.

...the pace of the downturn has surprised several economists, including Ian Shepherdson of High Frequency Economics. "The speed of the collapse has been astonishing," Shepherdson says. "This time last year, single-family home prices were up 16.4%. With inventory still rising, there is no chance of any short-term relief. Prices and volumes have a long way to fall."

Anyway, then some words of new-found wisdom from our buddy David Lereah:

To bring buyers back into the market, sellers simply have to lower their prices, said David Lereah, the NAR's chief economist.I think I just threw up a little bit.

Lereah has repeatedly cut his forecast for the housing market this year and says he's now unsure how deep the correction will turn out.

"If we have prices drop for the rest of the year and sales also continue to drop, then we will have a bad situation in housing of balloons popping rather than air coming out," Lereah said.

Either way, he says, "It's a buyer's market."

IMO what Lereah meant to say there at the end is 'sellers are screwed'. Ah, and he's talking about 'popping balloon' now. I can't wait for when he utters "bubble". And he doesn't know where the bottom is? Maybe this will give him a clue:

{kind=link}

From Today's Marin IJ

From today's Marin Independent Journal:

Another nice thing about this IJ article is that it makes it pretty clear that what is happening in Marin's real estate market is really the same thing as what is happening in all other CA bubble markets; if it weren't for all the "Marin is special/different" crap I wouldn't feel the need to say it.

And a plea:

"The fact is that Realtors do not set price and, in the end, the sellers do not set the price, either," Nielsen [a Marin Remax realtor] said. "Buyers do, and often it takes time for sellers to accept that reality."Like I've been repeatedly saying, you buyers are in the driver's seat now. You are driving this market and you always have been. Take this market to where you want it to be.

Another nice thing about this IJ article is that it makes it pretty clear that what is happening in Marin's real estate market is really the same thing as what is happening in all other CA bubble markets; if it weren't for all the "Marin is special/different" crap I wouldn't feel the need to say it.

Buyers are holding out to see if prices fall further.Stop "holding out". That just causes the market to languish and increases the time duration of the pain. You need to low-ball. Buyers set the prices, not the sellers. And IMO don't go in for the incentives nonsense (paying closing costs, a new car, one year subscription to some spa, etc.). All that matters is the sale price -- this market is going to be bad for years and so you have to count on owning that new house for years. So think about the longer term costs like property taxes. And disregard staging. Imagine that staged home as how it will look after you have actually lived in it for awhile.

"It is definitely a buyer's market, no two ways about it," said Jim Wilson, an analyst with JMP Securities in San Francisco. "This idea that prices don't go down is nonsense."Now they tell us. So what was all that "housing never goes down" stuff? Gibberish? Ok, rhetorical question I admit.

And a plea:

In Marin County, "the whole reason I think that we are seeing any kind of slowdown at all is because sellers are still pricing as if we are in an appreciating market, and we are not," Frank Howard Allen Realtor Kathleen Clifford said. "My message to sellers is be realistic, price your house appropriately and it will sell. If you have not priced it appropriately, for God's sake, take a price reduction."That's right, let's get the snowball rolling.

Monday, September 25, 2006

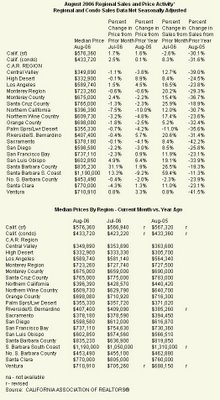

The C.A.R. on the August, 2006 Results

So sayeth the C.A.R.:

Home sales decreased 30.1 percent in August in California compared with the same period a year ago, while the median price of an existing home increased 1.6 percent, the CALIFORNIA ASSOCIATION OF REALTORS® (C.A.R.) reported today.Anticipated by who exactly? Not the C.A.R. At least not publicly. And what do you mean exactly by "initial stages"? This "adjustment" will last years.

“We experienced the greatest year-to-year sales decline last month since August 1982, when sales fell 30.4 percent,” said C.A.R. President Vince Malta. “This is another indication that we’re in the initial stages of a long-anticipated adjustment in the market.

“Buyers today have a much greater selection of properties from which to choose, while some sellers are still clinging to price expectations that are no longer valid in today’s market,” he said.Sounds familiar.

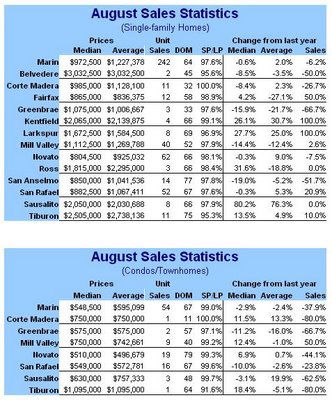

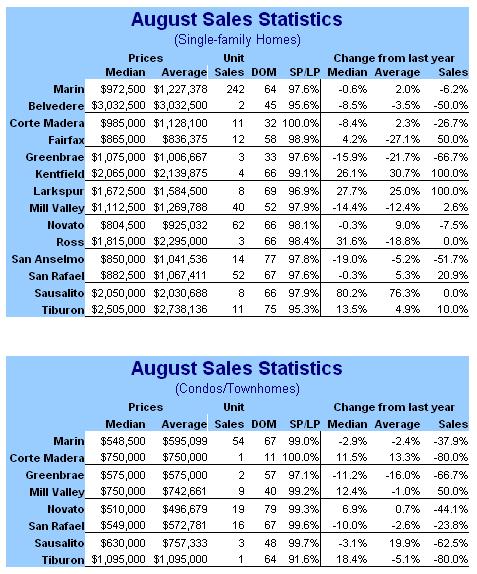

“Although the median price in the state and in several regions hit an all-time record in August, we expect softer prices toward the end of the year,” said C.A.R. Vice President and Chief Economist Leslie Appleton-Young. “The median price typically peaks somewhere between June and August before declining toward the end of the year. Some areas of the state already have experienced year-to-year declines for more than two months. This is in stark contrast to the past several years when there were constant double-digit increases. The long-term trend remains to be seen.”Sounds familiar. Below is their charted data:

Marin Market Observations by a Local Agent

The latest newsletter from Marin real estate agent Liz McCarthy is out. According to her Marin remains in a "strong buyer's" market what with only 19.2% of listings in contract.

I have spoken at great length with Ms. McCarthy and have found her to be a very honest, forthright, and buyer-centered agent. The fact that she makes a serious effort to compile some statistics is also praiseworthy IMO. I have featured her data before on this blog. Please check out her site and offer any suggestions that you might have to improve it (since she asks for such feedback) as she is clearly committed to providing the best service that she can.

The following comments by Ms. McCarthy I found interesting. This first one bolsters my impression that what has been selling at asking price are the "spotless" houses (the nicest of the nice) and the very expensive houses (purchased by people for whom the increase in interest rates have not (yet) had an effect). Thus, the median/average statistics routinely reported in the main stream media may not be at all reflective of what is actually going on in the market and should be considered more as an indication of the mixture of houses that are selling instead of as a measure of what the average house would sell for. It seems to me quite possible that there is a serious correction going on in the "low end" Marin housing market whereas the "high end" is not yet correcting even though the median/average price statistic is flat, or slightly up, or slightly down during any given month. I will try to nail down this last point with some data later.

I have spoken at great length with Ms. McCarthy and have found her to be a very honest, forthright, and buyer-centered agent. The fact that she makes a serious effort to compile some statistics is also praiseworthy IMO. I have featured her data before on this blog. Please check out her site and offer any suggestions that you might have to improve it (since she asks for such feedback) as she is clearly committed to providing the best service that she can.

The following comments by Ms. McCarthy I found interesting. This first one bolsters my impression that what has been selling at asking price are the "spotless" houses (the nicest of the nice) and the very expensive houses (purchased by people for whom the increase in interest rates have not (yet) had an effect). Thus, the median/average statistics routinely reported in the main stream media may not be at all reflective of what is actually going on in the market and should be considered more as an indication of the mixture of houses that are selling instead of as a measure of what the average house would sell for. It seems to me quite possible that there is a serious correction going on in the "low end" Marin housing market whereas the "high end" is not yet correcting even though the median/average price statistic is flat, or slightly up, or slightly down during any given month. I will try to nail down this last point with some data later.

Interestingly enough, homes again priced under $500,000 are sitting on the market longer and are currently in a “Strong Buyers” Market whereas homes priced from $500,000 to 999,000 are in a “Buyers Market”. Again, like last month I find it very interesting to note that homes priced from $2,500,000 to $2,999,999 are in a “Balanced Market!” To me, this seems to mean that buyers in the higher end of the Marin real estate market are not affected as much by the increase in interest rates, as they are more likely to be making their home purchases with more cash as compared to mortgages.It is nice to see agents point out deficiencies with the stats compiled from the MLS:

I’ve decided to no longer track the Sold price changes as compared to the original list price based on DOM. The reason for this is that I’ve just discovered that our MLS system’s way of calculating these stats are not really accurate. Their stats show very little price drop even over time (around 5%), BUT these price changes only reflect the price SOLD compared to the last price change that was made NOT the original list price!!! So basically, overall the price drops are not accurately reflected in these comps. I will list them (based on our MLS way of calculating them) this month, but will no longer track the data.And a request for improvement:

And for those of you who do read these stats, I’d love to know that you find the information useful! It actually takes me quite a lot of time to track, compile and post the data each month – and I’d love to know that it is being utilized! Send me an email to let me know you like getting it!My main recommendation to Ms. McCarthy is for her to try and compile her stats on a consistent schedule. If you look back at her previous newsletters her stats are made for differing points in the month which makes month-to-month comparisons problematic.

What Do You Want?

I don't consider myself "obsessed" with Warren; not even a little. He just opened himself up as an opportunity to focus on Marin real estate agents whose ethics/motivations are questionable. That is an avenue that I had not explored much before. At the very least he shows that even "God's Country" has them. I think that is fair game. If I could weed out all of the depraved agents in Marin, I would.

On the flip side, the topic of slimy Marin RE agents has me thinking about explicitly promoting on this blog Marin agents who seem to be uncharacteristically honest and forthright and, importantly, who have the buyer's best interests in mind. The theory: reinforce good, honest behavior and punish bad, dishonest behavior. Unfortunately, my list is rather short so I doubt I'll make much headway on that effort.

But message received.

But please keep in mind that this blog is free. No one is forcing you to read it. I am grateful that you do, of course. This is my weblog of the Marin real estate bubble and what it means to me, what I think is interesting, what concerns me, and in general what I care about.

But having said that.... what do readers want to see on this blog? I ask this question because the first phase of this blog was to argue that there is a housing bubble (in general) and that it has "floated our boats" in Marin (in particular) as much as any other bubble market. I think there is general agreement now that is the case. But what next? Documenting the inevitable painful slide in Marin's housing market? More Marin myth-busting via poignant examples? More of the same, just minus Warren? What?

An honest question deserves an honest answer/constructive criticism.

On the flip side, the topic of slimy Marin RE agents has me thinking about explicitly promoting on this blog Marin agents who seem to be uncharacteristically honest and forthright and, importantly, who have the buyer's best interests in mind. The theory: reinforce good, honest behavior and punish bad, dishonest behavior. Unfortunately, my list is rather short so I doubt I'll make much headway on that effort.

But message received.

But please keep in mind that this blog is free. No one is forcing you to read it. I am grateful that you do, of course. This is my weblog of the Marin real estate bubble and what it means to me, what I think is interesting, what concerns me, and in general what I care about.

But having said that.... what do readers want to see on this blog? I ask this question because the first phase of this blog was to argue that there is a housing bubble (in general) and that it has "floated our boats" in Marin (in particular) as much as any other bubble market. I think there is general agreement now that is the case. But what next? Documenting the inevitable painful slide in Marin's housing market? More Marin myth-busting via poignant examples? More of the same, just minus Warren? What?

An honest question deserves an honest answer/constructive criticism.

Saturday, September 23, 2006

My Comment Left on Warren Carreiro's Blog

Warren Carreiro, that Marin real estate broker featured a while ago on this blog, seems to be deleting any and all comments left on his blog that contains a URL to my blog. That's his choice of course but I have to wonder of what Warren is afraid. Apparently, Warren is content with bad-mouthing a blog without actually providing a reference to the blog he is referring to and thereby allowing his readers to form their own opinions. Well, that's a blog owner's prerogative.

Warren Carreiro, that Marin real estate broker featured a while ago on this blog, seems to be deleting any and all comments left on his blog that contains a URL to my blog. That's his choice of course but I have to wonder of what Warren is afraid. Apparently, Warren is content with bad-mouthing a blog without actually providing a reference to the blog he is referring to and thereby allowing his readers to form their own opinions. Well, that's a blog owner's prerogative.I found a post on Warren's blog where one of my data plots is mentioned. Based on what some commentors were saying I decided I needed to clarify some potential misunderstandings on the part of the reader. Since I am not sure if my comment will actually get posted to Warren's blog (comment moderation is turned on), I thought I would post a picture of my comment here since it would be of benefit to readers of this blog as well:

Friday, September 22, 2006

Eyes Wide Shut

California and Marin house owners are slowly coming back to their senses following a prolonged period of debt-induced intoxication and I seriously doubt that they will like what they see (underlining is mine):

California and Marin house owners are slowly coming back to their senses following a prolonged period of debt-induced intoxication and I seriously doubt that they will like what they see (underlining is mine):[Says one California seller] “We have to be competitive, and we can’t be greedy,...It seems like people are afraid to buy now. They don’t know where the bottom is." Real estate agents and economists say Sterbens, and thousands of other sellers, may have to consider further reductions.No, "the only upside" is that many California towns have turned from a grotesquely unaffordable sellers' market to a fence-sitters' market. We here in Marin are still dealing with seller denial and significant hubris and so it will just take a little longer for us is all. A 5-10% drop in price is a very long way from what any California or Marin fence-sitter will enjoy. Why buy now at the inflection point ("the cusp of a long-feared correction")? Why buy if the price is going down? Think of all the money you would save, not just in terms of the down payment, but also in terms of taxes year after year. As prices come down and your savings increase, you could spend that money (that you actually earned yourself) to live instead of paying an overly inflated mortgage. Or you can use the savings to make an even larger down payment in the future, assume an even smaller loan, and actually afford to retire one day without being dependent on housing speculation. Or buy an even bigger, more grand place if that's your thing.

‘We’ve got sellers out there who have not adjusted to the new reality,’ said (realtor) Carla Giustino.

The only upside is that many California towns have turned from unaffordable hamlets to buyers’ markets.

Fresh data show that California’s market is not immune, and may be on the cusp of a long-feared correction. ‘I could see some continuing declines at least over the next 12 months,’ said economist Stephen Levy,. ‘Typically sellers begin to lower their prices, and that’s when you worry that the bottom could drop out. We still haven’t reached that point, but I don’t see how the economy can continue with these prices.’

The median price last month in San Mateo County was $721,000, down from $773,000 a year ago. The median home price in Marin County last month was $803,000, down from $822,000 in August 2005 [a 2.3% YOY price decline]. San Diego and Alameda counties also saw prices decline.

The median Marin County home is nearly four times the national median [but our median income is not four times the national median income], and agents say that's made some locals oblivious to the downward pressure. Too often, they're pricing their homes higher than comparable homes in their zip code, and they still expect bidding wars and multiple offers.

"We've got sellers out there who have not adjusted to the new reality," said Carla Giustino of Greenbrae-based Frank Howard Allen Realtors. Giustino urges clients with homes worth $1 million or more to drop prices by $50,000 to $100,000.

A lot of recent buyers were willing to pay prices that they knew perfectly well were ludicrous only because of their expectation of greater future appreciation. Many extracted equity (borrowed against the assumed future sale price) to live a lifestyle now, today that they couldn't otherwise afford and were not willing to wait for when the day came to actually sell the house. They now want you, the buyer, to pay for that lifestyle. Don't believe me? Check out this poor fellow (found on the Housing Panic blog). He's only 24 years old and our massively screwed up lending system actually lent him millions of dollars to buy seven properties in various states; he is now over two million dollars in debt and facing foreclosure. This may be an extreme and certainly very sad example but I fear not an uncommon one as we will be hearing more and more such stories. Just look at all the "investment" properties suddenly being sold in Sonoma, Napa, Tahoe, etc. As sorry as we may feel about people like this 24-year-old, should we really bail them out by buying their still obscenely price-inflated houses? Should you repeat their mistake of paying too much or does charity play a role in what you are willing to pay for a house? Or should you wait and buy when their asking prices are more appropriate? You buyers are starting to face some tough questions. The choice seems obvious, but that's just me.

So where are we in the Kübler-Ross sequence? Some are at the anger stage, others are still in denial, and still others may now be bargaining.

You buyers are firmly in the driver's seat now. Do you want to bring this market down faster? Here's how.

Thursday, September 21, 2006

REO In Novato

Bank owned sold in as-is condition.Single level- living rm. W/cathedral ceilings, kitchen w/breakfast area. Family rm. W/fireplace. Formal dining. Master suite w/patio access. Great patio area and dark bottom pool. Rv/boat parking along side of house. Close to shopping, transportation& schools.This 3 br 2 ba house is in Novato. Built in 1974, 1712 sq ft. No significant upgrades that I can see. Current asking price is $649,900.

Sales history:

02/22/2002: $440,500The loan history summary paints a pretty clear and sad picture -- the last owners of this house HELOCed out about $160,000 in equity and moved from a fixed rate conventional loan into a variable rate loan. One can only surmise that when their variable rate reset they could no longer make the payments and so they lost the house to the bank in foreclosure. The bank assumed it with a value of $585,650.

02/26/1998: $309,000

Yes, it happens even in Marin.

Sorry about not being able to find a picture of the exterior of this house.

BAREIS Stats and the Warren Saga

Perhaps contrary to what you might think, I am actually on good speaking terms with some Marin real estate agents/brokers and some of them even approve of what I am doing on this blog.

One Marin agent mentioned today by email that there are some problems with some of the statistics coming out of BAREIS. Here is the relevant portion of an email sent to me (reproduced with permission):

Also, the Warren Carreiro saga continues: a reader emailed me today telling me that he keeps trying to leave a comment on Warren's blog -- a comment containing this blog's URL so that readers of Warren's blog know what the heck Warren is complaining about. But Warren keeps deleting those comments and is now moderating comment submissions. Hey Warren, what are you afraid of?

One Marin agent mentioned today by email that there are some problems with some of the statistics coming out of BAREIS. Here is the relevant portion of an email sent to me (reproduced with permission):

Just found out something that you might find interesting:

% price change vs. sold (according to BAREIS) isn't accurate….it's based on list price compared to the most recent price when the property closed NOT the original list price. I just started tracking those stats, but I now think they are worthless with this new info, it means that % price drop is much more than indicated…. I will no longer track these stats unless BAREIS fixes this stat.

I found this out because I'm on the Marin Association of Realtors Technology board and we often times communicate problems to BAREIS.

Also, the Warren Carreiro saga continues: a reader emailed me today telling me that he keeps trying to leave a comment on Warren's blog -- a comment containing this blog's URL so that readers of Warren's blog know what the heck Warren is complaining about. But Warren keeps deleting those comments and is now moderating comment submissions. Hey Warren, what are you afraid of?

Wednesday, September 20, 2006

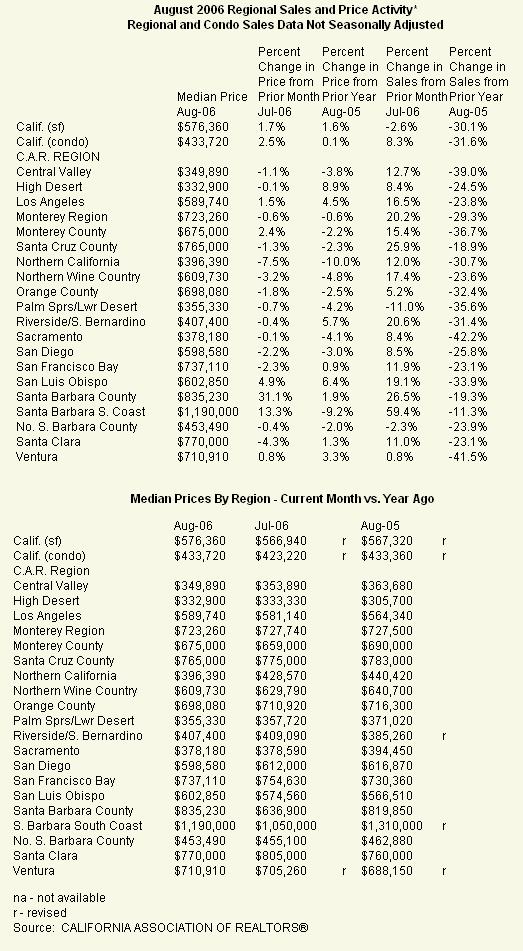

DataQuick Results for August, 2006

Source.

Quote of note:

"Several things are going on. Many homes are being offered for sale at unrealistically high prices as sellers try to game the peak of the market. Buyers appear to be taking a wait-and-see approach as sellers get real with their asking prices. The market seems to be going into a lull, until this all shakes out. It does appear that the strong appreciation of the recent past is leveling off," said Marshall Prentice, DataQuick president.

Tuesday, September 19, 2006

Tiburon DOM Map

A reader sent this in (thank you):

Hey there.

After hearing arguments asserting how much wealth is driving "prime" SFBay real estate values, I thought I'd do a little research. While many have a general feel for how long property is sitting, I thought I'd graphically illustate the hard truth for an undisputed "prime" market. The attached file is a direct screen dump from Ziprealty's map search feature, displaying all home listings for Tiburon area--with DOMs added in black. No "cherry picked" data here, and people can make their own conclusions. If you find this compelling, post it to the blog.

Schiff Video - 5 Years of Appreciation to be Erased

Euro Pacific Capital's Chief Global Strategist Peter Schiff predicts a recession in 2007 and argues in this Bloomberg video (19 minutes duration; give it time to load) that 'All of the home price appreciation of the last 5 or 6 years will be erased.' I loved seeing the interviewer spew the popular talking points and then squirm in response to Schiff's reasoning.

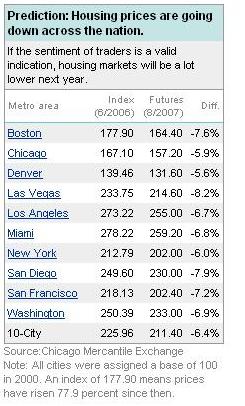

Futures Trading Bets On Housing Drop

Investors are betting that real estate is going down as indicated in this article:

Investors are betting that real estate is going down as indicated in this article:Home prices will be lower a year from now in the nation's leading markets - at least that's what investors speculating on residential real estate believe.And I thought the info contained in the next graphic from that same article for San Francisco was interesting:

The S&P CME Housing Futures and Options, launched this past spring, enable investors to hedge against a drop in the value of residential properties in the future or to bet that those values will go up.

The investments are tied to the the Case-Shiller Home Price Indices. According to Robert Shiller, author of "Irrational Exuberance," the results of the trading in housing futures have substantial predictive value. "It gives us a finger on the pulse of the markets," he says. "We've never had that before."

The median family income in SFO is $70,772 yet family purchasing power is only 48% of that as compared to 89% on average for all other "best" places to live. SFO's job growth is a negative -7.23% from 2000 to 2005 whereas it is a positive 10.97% for the average of the other "best" locations. Despite that, housing prices increased 14% from 2004 to 2005.

The median family income in SFO is $70,772 yet family purchasing power is only 48% of that as compared to 89% on average for all other "best" places to live. SFO's job growth is a negative -7.23% from 2000 to 2005 whereas it is a positive 10.97% for the average of the other "best" locations. Despite that, housing prices increased 14% from 2004 to 2005.Welcome to the Bay Area where you can earn a princely income but you must live like a pauper (unless your house keeps appreciating at double digit rates year after year allowing you to make up for the shortfall with a nice HELOC).

Monday, September 18, 2006

Flip This

So you still don't believe that there are flippers in Marin or that housing won't always make you a gazillionaire even in Marin where everyone wants to live? Well, here's another one:

I first blogged this Mill Valley POS back in December of 2005. Back then they were asking $745,000 for this tiny (699 sq ft, 2 br 1 ba, built 1923) house right on Shoreline Hwy. and across the street from the 7-11. After lingering on the market for months they reduced the asking price to $675,000 and after lingering some more they (apparently) took it off the market. It's too bad I didn't record the days on market statistic as it's been wiped out along with the price reduction history. Anyway, it has recently been relisted at the same reduced asking price of $675,000.

I first blogged this Mill Valley POS back in December of 2005. Back then they were asking $745,000 for this tiny (699 sq ft, 2 br 1 ba, built 1923) house right on Shoreline Hwy. and across the street from the 7-11. After lingering on the market for months they reduced the asking price to $675,000 and after lingering some more they (apparently) took it off the market. It's too bad I didn't record the days on market statistic as it's been wiped out along with the price reduction history. Anyway, it has recently been relisted at the same reduced asking price of $675,000.

The current owners purchased the property for $480,000 on July 1, 2005. That's a "fair" price as it's assessed value at that time was $486,500 according to the loan history summaries that I've seen. The $480,000 purchase price also happens to be exactly how much their variable rate loan was for. (Can anyone say "no money down loan"?) They took out an additional $200,000 (it says "refi" but how can that be unless they were able to get a much better appraisal?) presumably to do some improvements which the listing description describes to some extent. So they are on the hook for a total of $680,000. After "owning" it for just 4 to 5 months they hoped to flip it for a quick profit. Now, however, they are trying to sell it again at the same reduced asking price of $675,000 and are basically trying to break even (actually a small loss, relatively speaking).

I don't know why they think they can get their asking price when they failed to get it before and they haven't done anything new to the property as far as I can tell; the market certainly hasn't improved since then.

Update 10-10-2006: Thanks to the sharp eyes of an attentive reader I can report that the current "owners" of this house are now asking $638,995 which is a 14% price reduction from the original asking price of $745,000. The sellers are trying their hardest not to bring a check to closing.

I first blogged this Mill Valley POS back in December of 2005. Back then they were asking $745,000 for this tiny (699 sq ft, 2 br 1 ba, built 1923) house right on Shoreline Hwy. and across the street from the 7-11. After lingering on the market for months they reduced the asking price to $675,000 and after lingering some more they (apparently) took it off the market. It's too bad I didn't record the days on market statistic as it's been wiped out along with the price reduction history. Anyway, it has recently been relisted at the same reduced asking price of $675,000.

I first blogged this Mill Valley POS back in December of 2005. Back then they were asking $745,000 for this tiny (699 sq ft, 2 br 1 ba, built 1923) house right on Shoreline Hwy. and across the street from the 7-11. After lingering on the market for months they reduced the asking price to $675,000 and after lingering some more they (apparently) took it off the market. It's too bad I didn't record the days on market statistic as it's been wiped out along with the price reduction history. Anyway, it has recently been relisted at the same reduced asking price of $675,000.The current owners purchased the property for $480,000 on July 1, 2005. That's a "fair" price as it's assessed value at that time was $486,500 according to the loan history summaries that I've seen. The $480,000 purchase price also happens to be exactly how much their variable rate loan was for. (Can anyone say "no money down loan"?) They took out an additional $200,000 (it says "refi" but how can that be unless they were able to get a much better appraisal?) presumably to do some improvements which the listing description describes to some extent. So they are on the hook for a total of $680,000. After "owning" it for just 4 to 5 months they hoped to flip it for a quick profit. Now, however, they are trying to sell it again at the same reduced asking price of $675,000 and are basically trying to break even (actually a small loss, relatively speaking).

I don't know why they think they can get their asking price when they failed to get it before and they haven't done anything new to the property as far as I can tell; the market certainly hasn't improved since then.

Update 10-10-2006: Thanks to the sharp eyes of an attentive reader I can report that the current "owners" of this house are now asking $638,995 which is a 14% price reduction from the original asking price of $745,000. The sellers are trying their hardest not to bring a check to closing.

Sunday, September 17, 2006

A Great Marin Realtor Rant

There's a great rant by a Marin realtor in "The Warren" post. Go check it out. It's the one posted on 9/17/2006 07:00:00 AM.

Saturday, September 16, 2006

Watching Seller Psychology in San Rafael

This is that San Rafael house that was featured in a New York Times article back in early May; I've blogged it before (here and here). I like to keep an eye on it from time to time since it seems like a good candidate for watching seller psychology in action during a classic post frenzy downturn. It seems like they are chasing the market down. Maybe other sellers could learn from this example.

This is that San Rafael house that was featured in a New York Times article back in early May; I've blogged it before (here and here). I like to keep an eye on it from time to time since it seems like a good candidate for watching seller psychology in action during a classic post frenzy downturn. It seems like they are chasing the market down. Maybe other sellers could learn from this example.Their most recent drop in price puts the total price reduction at 14%:

Price Reduced: 04/11/06 -- $1,045,000 to $997,500 (-4.5%)Sales history (updated from my previous post):

Price Reduced: 05/05/06 -- $997,500 to $949,000 (-5%)

Price Reduced: 06/12/06 -- $949,000 to $939,000 (-1.1%)

Price Reduced: 08/30/06 -- $939,000 to $899,000 (-4.3%)

FWIW, Zillow.com's "Zestimate": $787,682

02/27/2006: $700,000Based on the publicly available loan information that I've seen, it seems that this property is owned by someone who actually resides in Sebastopol.

05/14/2004: $735,000

The last purchase in February, 2006 for $700,000 used a variable rate loan. It looks like they took out an additional $200k (for improvements?). So these "owners" are looking to break even at this point (but after taking into consideration closing costs and any carrying costs they are actually looking at a loss).

So this would appear to be a classic flip. Yep, it happens even in Marin.

Update: I forgot to mention that the previous owners did multiple cash-out refis on their variable rate loan.

Friday, September 15, 2006

"Spotless"

Update 9-16-06: I added an inventory graph.

If you have a spotless house in a spotless location, then you will probably get your asking price. Everyone else must cut the price to sell which most sellers are still loath to do. That's why the recent median/average sales prices have at times deceptively inched up in an overall environment of price reductions; these days the median/mean reflects the mixture of houses that sell and not a measure of the average price of the market as a whole. This article in SF Gate supports that conclusion.

If you have a spotless house in a spotless location, then you will probably get your asking price. Everyone else must cut the price to sell which most sellers are still loath to do. That's why the recent median/average sales prices have at times deceptively inched up in an overall environment of price reductions; these days the median/mean reflects the mixture of houses that sell and not a measure of the average price of the market as a whole. This article in SF Gate supports that conclusion.

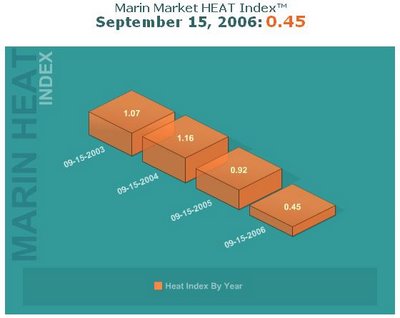

Here's the discussion for the above picture by the author of the HEAT Index:

Here's the discussion for the above picture by the author of the HEAT Index:

Here's the August, 2006 results according to Vision RE. It looks like everyone in their sample of the overall market rushed in at the last minute to complete those sales in time for the start of school. Or maybe it was an effect of lowered interest rates (oh, but wait a minute, people in Marin are supposed to be so wealthy that interest rates don't really matter). It will be interesting to see what DataQuick comes in with:

If you have a spotless house in a spotless location, then you will probably get your asking price. Everyone else must cut the price to sell which most sellers are still loath to do. That's why the recent median/average sales prices have at times deceptively inched up in an overall environment of price reductions; these days the median/mean reflects the mixture of houses that sell and not a measure of the average price of the market as a whole. This article in SF Gate supports that conclusion.

If you have a spotless house in a spotless location, then you will probably get your asking price. Everyone else must cut the price to sell which most sellers are still loath to do. That's why the recent median/average sales prices have at times deceptively inched up in an overall environment of price reductions; these days the median/mean reflects the mixture of houses that sell and not a measure of the average price of the market as a whole. This article in SF Gate supports that conclusion.[Regarding the RE market in SFO] "It's cratering underneath my feet," muttered one agent after his pristinely marketed, cautiously priced listing engendered only a single, below-asking offer. Another agent, whose characteristic optimism had evaporated like the sheen on a new floor after an open house, bluntly described the market as "flat-lined" in his newsletter.The Marin HEAT Index is at yet another new all time low of 0.45. Any bets on what it will be by Thanksgiving?

What exactly constitutes a "spot"? Every agent I spoke to gave me lists of fatal flaws, and many of these lists overlapped. Unfortunately, most of the flaws are out of a seller's control: bad location (across the street from a housing project, bus stop or other "undesirable" vista), no parking, massive foundation problems, no outdoor space.

Other, less-permanent flaws may scare buyers off because they seem too daunting to fix. Having only one bathroom, for instance, is often enough to besmirch the loveliest of properties. Likewise, many a buyer can't envision fixing an awkward floor plan or popping windows into an irredeemably dark house.

Indeed, the concept of move-in condition has gained increasing traction, especially among more affluent buyers searching for $1 million-plus homes. "I'm seeing a real resistance to renovating," says Sotheby's Gloria Smith. "They've done it and seen their friends do it. They know what kind of stress it puts on a marriage and the fact that the contractor's costs often double."

According to the majority of agents, it's not worth scrimping when it comes to improving surfaces. The new standard has gone far beyond vacuuming the rug and doing the dishes before prospective buyers arrive.

During the boom, buyers just wanted a roof over their heads. Now it seems they want every little thing on their "under heaven" wish list. But short of that, agents say, they'll settle for that lovin' feelin' that only a buyers' market can bring.

"Buyers want a good deal," says Shagley. "They want to feel as if they've gotten something for their money."

Who can blame them?

Here's the discussion for the above picture by the author of the HEAT Index:

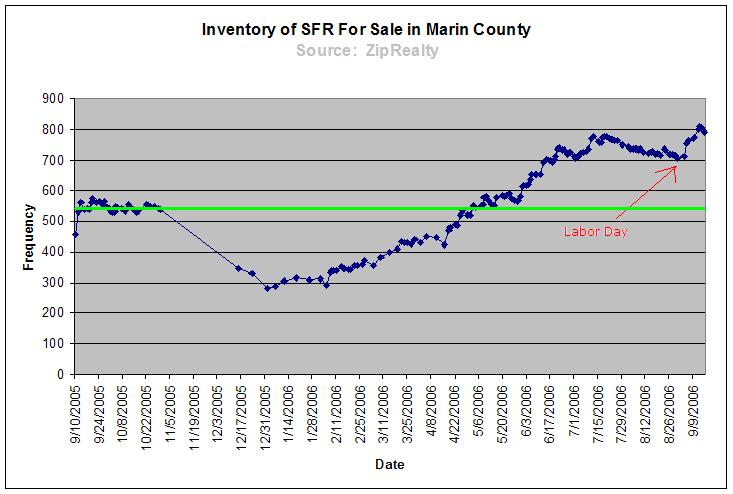

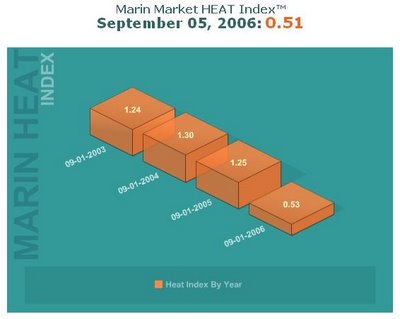

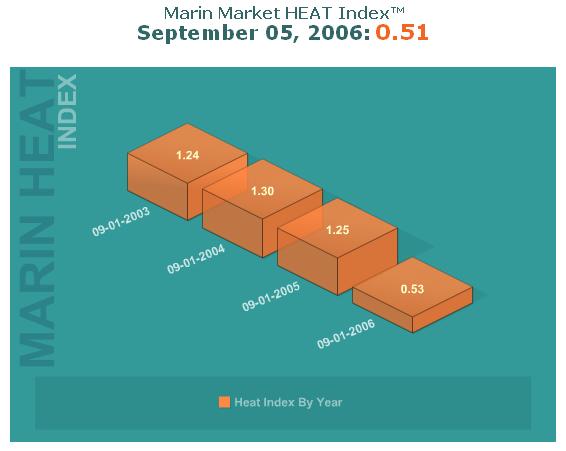

Here's the discussion for the above picture by the author of the HEAT Index:My September 1 prediction that the market and the Market HEAT Index would continue to cool through early and mid-September was accurate. More listings, lower rates for closed sales and for pending sales combine into a pretty frosty Marin market. Larkspur is the only town showing a "Balanced Market" index reading, and the price range of $2 Million - $4 Million is the only range performing at or above the previous year's levels. Look at these statistics:And according to ZipRealty Marin's SFR inventory is currently about 45% higher (refer to green line in the following figure) than it was this time last year (my search parameters were any SFR within the asking price range of $100,000 and $10,000,000, any number of bathrooms, bedrooms, etc., in any Marin town):My prediction that the Index would experience a rise by early and mid-October is unlikely to pan out, however, because of the decrease in pending sales to the very low level registered on the 15th. (It was 265, down 9% from the reading on September 1.) This presages a further reduction in the Marin Market HEAT Index well into October and early November.

- The Market Heat Index for Marin declined from 0.53 to 0.45 (a new record cool point);

- Pending sales declined from 291 to 265;

- Number of properties sold in prior 30 days was essentially unchanged (250 to 249); and

- Active, available for purchase properties increased from 1,019 to 1,143.

Buyers: I truly believe that buyers in Marin who act in a down market such as this are both bold and smart. They have lots of choices, and they have a lot of bargaining power. They almost always do well if they buy to hold.

Sellers: Sellers, though, need to work harder be more pragmatic about pricing their property then at any time here in the past ten years. Properties do sell, even in these quite cool conditions. But only occasionally do they sell over their asking price or with multiple offers. Good condition, fair-to-low asking price, good on-line marketing: these are the watch words for sellers in this market.

Here's the August, 2006 results according to Vision RE. It looks like everyone in their sample of the overall market rushed in at the last minute to complete those sales in time for the start of school. Or maybe it was an effect of lowered interest rates (oh, but wait a minute, people in Marin are supposed to be so wealthy that interest rates don't really matter). It will be interesting to see what DataQuick comes in with:

Thursday, September 14, 2006

My Master Plan to Enslave the World

It became apparent in a previous post that someone was on to me -- they realized that what I have been trying to do is to create a real estate bubble in Marin. That is not entirely correct. Puhleeze. I have in fact been striving to create a real estate bubble not only in the entire country but also over the entire face of the globe! Hannibal, Alexander, Caesar, Khan...they're all panzies by comparison.

It became apparent in a previous post that someone was on to me -- they realized that what I have been trying to do is to create a real estate bubble in Marin. That is not entirely correct. Puhleeze. I have in fact been striving to create a real estate bubble not only in the entire country but also over the entire face of the globe! Hannibal, Alexander, Caesar, Khan...they're all panzies by comparison.It would be an understatement to say that it has not been easy. You see, to pull this off I realized very early on that a shrewd understanding of human psychology was required. I know from personal experience that administering pleasure for a brief period of time and then abruptly taking it away only heightens that pleasure later when it is again applied. It's called "priming the system". Therefore, to accomplish my ultimate diabolical goal I had to first create the impression of great wealth and then abruptly take it way. So my evil plot began by engineering the tech bubble. This required talking to my buddies at the Fed to crank up the printing presses and flood the U.S. financial system with liquidity. They were all too happy to oblige as they owed me a few favors; Greenspan was my poodle you see. A few anonymous letters to Gates, Ellison, Jobs, etc. and the foundations of a tech bubble were laid.

Anyway, after the tech bubble got really hot and everyone and their brother fancied themselves a stock investing genius I told Greenspan to bring it to an end which he did. Unfortunately, the financial aftermath of the tech bubble collapse was a little harsher than I would have liked so Greenie (as I am fond of calling him) had to drop the over night lending rate to frighteningly low levels. Everyone was feeling really poor and thus desperately ready for the next bubble...the real one...The Big One...the Bubble to End All Bubbles...but those dang Muslim extremists had to go and try and spoil it for everyone. It was touch and go for a while and I thought I might fail but fortunately American ingenuity, economic flexibility, and all that economic dark matter floating around prevailed in the end. And Greenie's further dropping of the interest rates to the point of almost making money free didn't hurt either.

Once the system was holding it's own, Greenie's interest rates made the carry trade an obvious winner. All part of the plan my friends. Banks started lending to everyone as anticipated, even to corpses (I admit that I didn't see that one coming but it's all good)! What with the cheap money, all the tax savings associated with mortgages, etc. people were buying up houses like crazy as predicted. The fact that they are illiquid, depreciating assets didn't matter. The fact that fraud was rampant didn't matter either. And I knew I could count on denial, cognitive dissonance, self-justification, and the typical American's ignorance of history to supercharge the bubble to heights unseen. As a result, it got so frenzied it even scared me a little; sort of like how Dr. Frankenstein must have felt when his creation first rose from the slab..."it's alive, ALIIIIIIIIVE!". And everyone was so giddy with greed and so convinced that they were real estate investor geniuses that no one bothered to stop and think about it.

But chaining Americans to their mortgages wasn't enough you see. I needed more; something was missing. Ah, I know -- credit cards. American's love their credit cards almost as much as they love the TV. My connections in the credit card industry run deep and they agreed to give out cards like they were candy. And when I asked them to lobby for that bankruptcy law they were aquiver with delight. My pals in Congress caved like the spineless jellyfish they are (don't you just love America?) and now the final stage of my Master Plan is in place...crash the bubble, wipe out trillions in paper wealth, enslave the populace with debt that neither they nor their grandchildren will ever be able to repay, and do it the world over. This blog is but a means to an end you see. The noose is around the neck of America and I'm tightening it down. Almost there. And then you are mine.

Wednesday, September 13, 2006

More Marin RE Agent Bloggers

Blogging by real estate agents and brokers seems to be the new thing for some of them. I like the theme this Marin agent chose for her blog... reminds me of something...

I left a comment on her top (9/12/06) post with a link to this blog...let's see how long it lasts. I posted it today at 2:55 PM.

I left a comment on her top (9/12/06) post with a link to this blog...let's see how long it lasts. I posted it today at 2:55 PM.

Fed Bailouts and Modern Financial Slavery

And so it begins: this saga started as early as 2002! Can you imagine how bad it is going to get moving forward? Foreclosures are increasing at an alarming rate as I write.

And so it begins: this saga started as early as 2002! Can you imagine how bad it is going to get moving forward? Foreclosures are increasing at an alarming rate as I write.Antonio and Kathlene Mareno obtained a home mortgage from Dime Savings Bank. The terms of the mortgage required them to pay their property taxes directly to the local tax collector. However, if they failed to do so, the mortgage allowed the lender to pay the property taxes, add the property tax amount to the mortgage balance, and adjust the monthly mortgage payment.The Marenos are basically looking to get bailed out by the Federal government after failing with the State government. This sad story is going to be repeated over and over again in the coming months and years, only made worse by the new bankruptcy laws. Welcome to financial slavery and serfdom thanks to the housing bubble.

The borrowers allegedly failed to pay their property taxes for 2002 and 2003. As a result, Dime Savings paid the property taxes and increased the monthly mortgage payment from $754 to $1,268. The Marenos made one payment of $754 after the increase and then stopped making any mortgage payments.

In 2004, Dime Savings filed a complaint against the Marenos to foreclose on the mortgage. The state court then granted a summary judgment allowing the foreclosure.

Then in November 2005 the Marenos sued Dime Savings in U.S. District Court, alleging the state trial court's handling of their case violated their federal due-process rights. Dime Savings argued the foreclosure issue was already decided in the state court and the homeowners don't have a right to litigate the same issue again in federal court.

The Marenos already had their right to litigate and appeal the foreclosure judgment in state courts, the judge ruled. They failed to prove a federal denial of due-process claim, so this case is dismissed for lack of jurisdiction, and the foreclosure may proceed, the judge concluded.

Can there really still be people seriously thinking about buying at the top of this bubble market?

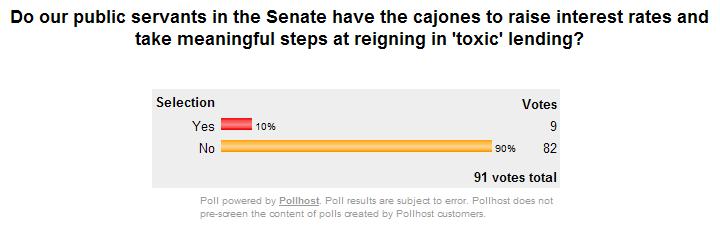

US Senate Hearings on the Housing Bubble

In case you haven't already heard, the US Senate hearings on the housing bubble (held in an open session of the Senate Banking Committee), entitled "The Housing Bubble and its Implications for the Economy", will be getting underway soon (you can find more info here). (And is it just me or are there no Californian representatives on the committee?) It will be interesting to see what, if anything, will come out of these hearings. Will they "conclude" that there is no housing bubble so it's business as usual? Will they cave to lobbying pressure from the NAR and others? Or will they find that there are sound bases for serious concern and move to a full-scale investigation? Are these hearings the first attempt at pre-election maneuvering and the covering of their collective political arses? Is this the start of figuring out who to blame, making a few indictments, and then shifting public focus to the latest crisis du jour?

In case you haven't already heard, the US Senate hearings on the housing bubble (held in an open session of the Senate Banking Committee), entitled "The Housing Bubble and its Implications for the Economy", will be getting underway soon (you can find more info here). (And is it just me or are there no Californian representatives on the committee?) It will be interesting to see what, if anything, will come out of these hearings. Will they "conclude" that there is no housing bubble so it's business as usual? Will they cave to lobbying pressure from the NAR and others? Or will they find that there are sound bases for serious concern and move to a full-scale investigation? Are these hearings the first attempt at pre-election maneuvering and the covering of their collective political arses? Is this the start of figuring out who to blame, making a few indictments, and then shifting public focus to the latest crisis du jour?The cynic in me is not expecting revelation. All these people are property owners and no doubt some of them have their fingers in the business side of real estate [unfounded speculation on my part]. The bottom-line is that they have a vested interest in seeing to it that property keeps getting more expensive. That fact will probably mean that if a problem is identified and a remedy is sought, that remedy will not involve forcing prices down to affordable levels. Instead what we will get are "band aid solutions" that sound good to constituents but have no real effect. The only real solution is to get out of the way, stop meddling with the market, and let it crash so as to get back on a healthy track.

Lawmakers behind Wednesday's hearing said that they were concerned that a steady flow of soft housing data could put the nation's economy in peril.

"The economy has been buoyed for some time by unrealistic expectations about the appreciation of housing prices," said Jack Reed, a Democrat from Rhode Island, who is helping sponsor the meeting. "Now that the housing market is cooling, the economy may be headed for a bumpy landing."

...the same committee will hold a hearing on the growth of innovative mortgage products that have mushroomed along with the housing sector.

The lawmakers will hear from several chief economists like Richard Brown of the Federal Deposit Insurance Corporation, Patrick Lawler of the Office of Federal Housing Enterprise Oversight, Dave Seiders of the National Association of Homebuilders and Tom Stevens of the National Association of Realtors.

I was planning on posting the above yesterday but the post about the Marin real estate broker in San Rafael was too much fun to watch unfold. Today, we now have some info about what is being said to the Senate by RE industry shills. No surprises. Here are some examples:

“For the past five years, the housing market has been a steadfast leader in the U.S. economy,” says Thomas Stevens, president of NAR, in testimony Wednesday before the U.S. Senate Subcommittee on Housing and Transportation and the Senate Subcommittee on Economic Policy. “After five years of outstanding growth, the housing market is undergoing a period of adjustment and becoming more and more of a balanced market between buyers and sellers.”"...a significant shift in interest rates or a change in the economy would change this forecast. NAR notes that a soft landing is possible under the right circumstances...". So in other words Mr./Ms. Senator, don't raise interest rates or crack down on "toxic" loan products or else houses will lose significant value.

“While recent developments raise concern, it is important to remember that the housing market varies significantly across the country,” Mr. Stevens says. One-third of the country (by population) is still seeing rising home prices, including Alaska, New Mexico, Vermont and many states in the South, excluding Florida, he says. But states like California that experienced the greatest increases in home prices in recent years are experiencing significantly lower sales, he says.

“Contrary to many reports, there is not a ‘national housing bubble,’” says Mr. Stevens. “We were seeing home prices and mortgage debt servicing cost-to-income ratios increase to unhealthy levels in some housing markets, which precipitate an adjustment.”

Also contributing to the cooling housing market is an increase in mortgage rates of nearly one point, speculative investors pulling back and first-time buyers being priced out of the market, the Realtors group says.

NAR warns that a significant shift in interest rates or a change in the economy would change this forecast. NAR notes that a soft landing is possible under the right circumstances and affordable mortgage financing is an important component in achieving this.

So I ask you:

It is not a surprise to me that these hearings are going on. What is surprising is that these hearings are happening now, so soon; usually you have to wait until the fecal matter hits the high RPM air pushing machine.

It is not a surprise to me that these hearings are going on. What is surprising is that these hearings are happening now, so soon; usually you have to wait until the fecal matter hits the high RPM air pushing machine.I think these hearings are a tacit admission that there is something terribly wrong in America today.

Monday, September 11, 2006

Local Broker Slams This Blog

Update 9/14/06: It looks like comments were turned back on at Mr. Carreiro's blog on 9/13/06 and remain on today.

Update 9/12/06 #2: As of at least 08:31:39 PM Mr. Carreiro has turned off the ability to leave comments on his blog.

Update 9/12/06: Mr. Carreiro has now turned on comments on his blog. Have at it.

Lander, owner of the Sacramento Land(ing) blog, brought to my attention Mr. Warren Carreiro's (a Marin real estate broker located in San Rafael) blog entry about me and my Marin Real Estate Bubble blog. Lander: thank you as this is priceless.

Lander, owner of the Sacramento Land(ing) blog, brought to my attention Mr. Warren Carreiro's (a Marin real estate broker located in San Rafael) blog entry about me and my Marin Real Estate Bubble blog. Lander: thank you as this is priceless.

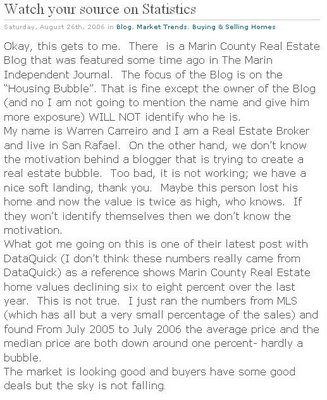

A screen shot of Mr. Carreiro's post about my blog follows (I chose to use a screen shot instead of my usual textual quote on the off chance that he decides to change his blog entry after reading this post):

Click on the image for a larger view.

Click on the image for a larger view.

Where to begin?

Well, first of all Mr. Carreiro says he doesn't want to link to my blog for fear of 'giving me more exposure'. If this blog is so terribly wrong, why would he be afraid of giving me more exposure? If anything, giving me more exposure would just make me look like a bigger fool than he thinks that I already am. And besides, what's wrong with having a forum in which people can freely express their opinions and share facts about Marin's real estate market? Isn't Mr. Carreiro agreeable to the idea of open and public debate and discussion on this topic? The last time I checked freedom of speech is still Amendment numero uno to the U.S. Constitution as written in the Bill of Rights. Maybe he really isn't in favor of open public discussion as I notice that he has comments turned off on his blog.

No, I think the real reason why Mr. Carreiro does not want to risk increasing my exposure is because he is threatened by me and my blog.

Mr. Carreiro then makes a point of reminding us that I have chosen to remain anonymous and that therefore he cannot determine my motivation... a "motivation behind a blogger that is trying to create a real estate bubble". First of all, my motivation is clear to anyone who has bothered to read my blog. Second of all, the claim that my blog could actually "create a real estate bubble" is ludicrous in the extreme and shows just how intellectually careless this individual is. I'm sorry, but there is no way one blog could affect a market in any significant way. Furthermore, if Mr. Carreiro had actually taken the time to read my blog, then it would be patently obvious to him that creating a housing bubble is the very last thing in the world that I would wish upon any community. And even if my blog could actually significantly affect the Marin housing market, does anyone really wonder why I might want to remain anonymous?

No, the real reason why people like him want to know my personal details is in the vain hope that they might find some conflict of interest or some bit of dirt that they could use to conveniently dismiss this blog. It's as simple as that. As discussed below, there is no conflict of interest nor is there any dirt.

Ok, moving right along... Mr. Carreiro then says "Maybe this person lost his home and now the value is twice as high, who knows". Yes, who knows? Certainly not you Mr. Carreiro. You know, I am really getting tired of people making up stories about me. First it was Jack McLaughlin and now this loser. No, on second thought I'm getting really pissed off about it. Some of these theories about me are getting just plain ridiculous and this one by Mr. Carreiro takes the cake. The reasons why I don't say much about myself are not only out of a sense of personal privacy, which I think any human being can appreciate, but also because such details are totally irrelevant. People should judge what I say on this blog based on the merits of what I say and not based on whether I own a house or how much money I've made or lost on my house. Unlike Mr. Carreiro, I have no financial stake whatsoever in the performance of our local housing market nor am I in any way affiliated with the housing industry in Marin. The means by which I make a living have absolutely nothing to do with real estate and as such is totally unaffected by how well real estate performs. My opinion about real estate is completely unaffected by how well Marin real estate performs which is more than I can say of Mr. Carreiro, a Marin real estate broker, whose livelihood is derived from selling real estate.

Furthermore, Mr. Carreiro seems to be claiming moral superiority vis-à-vis my anonymity by identifying himself by name. All I can do is scoff in disgust. Of course you identify yourself by name Mr. Carreiro...that's how you make a living for Christ's sake! If you didn't identify yourself on your blog and associate your name with the fact that you are a real estate broker, then you would be doing yourself a disservice as it would result in that much less business for yourself. Self-promotion is how people like you make a living.

Ok, next up... Mr. Carreiro questions that some of the latest numbers shown on this blog came from DataQuick. Now this really hurts as it strikes directly at my integrity. Never mind the fact that I provided a link...as I always do. Mr. Carreiro: did you actually read that blog entry? Here is my blog entry that Mr. Carreiro is talking about. And here is the link to DataQuick. Sorry to burst your bubble Mr. Carreiro, but according to DataQuick the Marin real estate market was down year-over-year -6.61% in July. I posted a screen shot of the relevant part of the table so that if that DataQuick page ever gets taken down (and my link to it goes stale), then at least we always have the screen shot.

I am, quite frankly, very offended that he seems to be implying that the numbers I have posted are a lie. I have never lied on my blog and I have absolutely no intention of ever lying on my blog. Doing so is counter to my purpose. I may make a mistake or two (I'm only human after all) but I do try hard to keep mistakes at a minimum. As for my opinion posts, well, they are just that...my opinion.

"...the sky is not falling." True. Not yet anyway.

Am I wrong? Share your thoughts.

If you would like to personally give Mr. Carreiro a piece of your mind, you will have to email him as comments have conveniently been turned off on his blog. You can find his email links in various locations on this page.

Update 9/12/06 #2: As of at least 08:31:39 PM Mr. Carreiro has turned off the ability to leave comments on his blog.

Update 9/12/06: Mr. Carreiro has now turned on comments on his blog. Have at it.

Lander, owner of the Sacramento Land(ing) blog, brought to my attention Mr. Warren Carreiro's (a Marin real estate broker located in San Rafael) blog entry about me and my Marin Real Estate Bubble blog. Lander: thank you as this is priceless.

Lander, owner of the Sacramento Land(ing) blog, brought to my attention Mr. Warren Carreiro's (a Marin real estate broker located in San Rafael) blog entry about me and my Marin Real Estate Bubble blog. Lander: thank you as this is priceless.A screen shot of Mr. Carreiro's post about my blog follows (I chose to use a screen shot instead of my usual textual quote on the off chance that he decides to change his blog entry after reading this post):

Click on the image for a larger view.

Click on the image for a larger view.Where to begin?

Well, first of all Mr. Carreiro says he doesn't want to link to my blog for fear of 'giving me more exposure'. If this blog is so terribly wrong, why would he be afraid of giving me more exposure? If anything, giving me more exposure would just make me look like a bigger fool than he thinks that I already am. And besides, what's wrong with having a forum in which people can freely express their opinions and share facts about Marin's real estate market? Isn't Mr. Carreiro agreeable to the idea of open and public debate and discussion on this topic? The last time I checked freedom of speech is still Amendment numero uno to the U.S. Constitution as written in the Bill of Rights. Maybe he really isn't in favor of open public discussion as I notice that he has comments turned off on his blog.

No, I think the real reason why Mr. Carreiro does not want to risk increasing my exposure is because he is threatened by me and my blog.

Mr. Carreiro then makes a point of reminding us that I have chosen to remain anonymous and that therefore he cannot determine my motivation... a "motivation behind a blogger that is trying to create a real estate bubble". First of all, my motivation is clear to anyone who has bothered to read my blog. Second of all, the claim that my blog could actually "create a real estate bubble" is ludicrous in the extreme and shows just how intellectually careless this individual is. I'm sorry, but there is no way one blog could affect a market in any significant way. Furthermore, if Mr. Carreiro had actually taken the time to read my blog, then it would be patently obvious to him that creating a housing bubble is the very last thing in the world that I would wish upon any community. And even if my blog could actually significantly affect the Marin housing market, does anyone really wonder why I might want to remain anonymous?

No, the real reason why people like him want to know my personal details is in the vain hope that they might find some conflict of interest or some bit of dirt that they could use to conveniently dismiss this blog. It's as simple as that. As discussed below, there is no conflict of interest nor is there any dirt.

Ok, moving right along... Mr. Carreiro then says "Maybe this person lost his home and now the value is twice as high, who knows". Yes, who knows? Certainly not you Mr. Carreiro. You know, I am really getting tired of people making up stories about me. First it was Jack McLaughlin and now this loser. No, on second thought I'm getting really pissed off about it. Some of these theories about me are getting just plain ridiculous and this one by Mr. Carreiro takes the cake. The reasons why I don't say much about myself are not only out of a sense of personal privacy, which I think any human being can appreciate, but also because such details are totally irrelevant. People should judge what I say on this blog based on the merits of what I say and not based on whether I own a house or how much money I've made or lost on my house. Unlike Mr. Carreiro, I have no financial stake whatsoever in the performance of our local housing market nor am I in any way affiliated with the housing industry in Marin. The means by which I make a living have absolutely nothing to do with real estate and as such is totally unaffected by how well real estate performs. My opinion about real estate is completely unaffected by how well Marin real estate performs which is more than I can say of Mr. Carreiro, a Marin real estate broker, whose livelihood is derived from selling real estate.